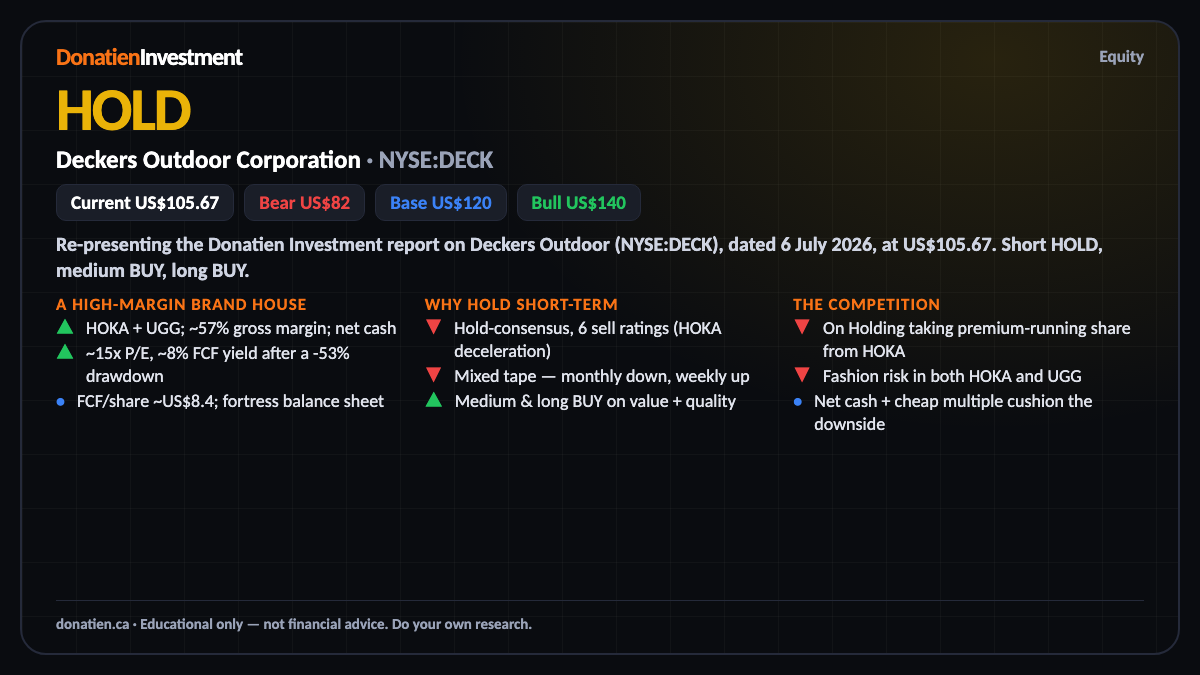

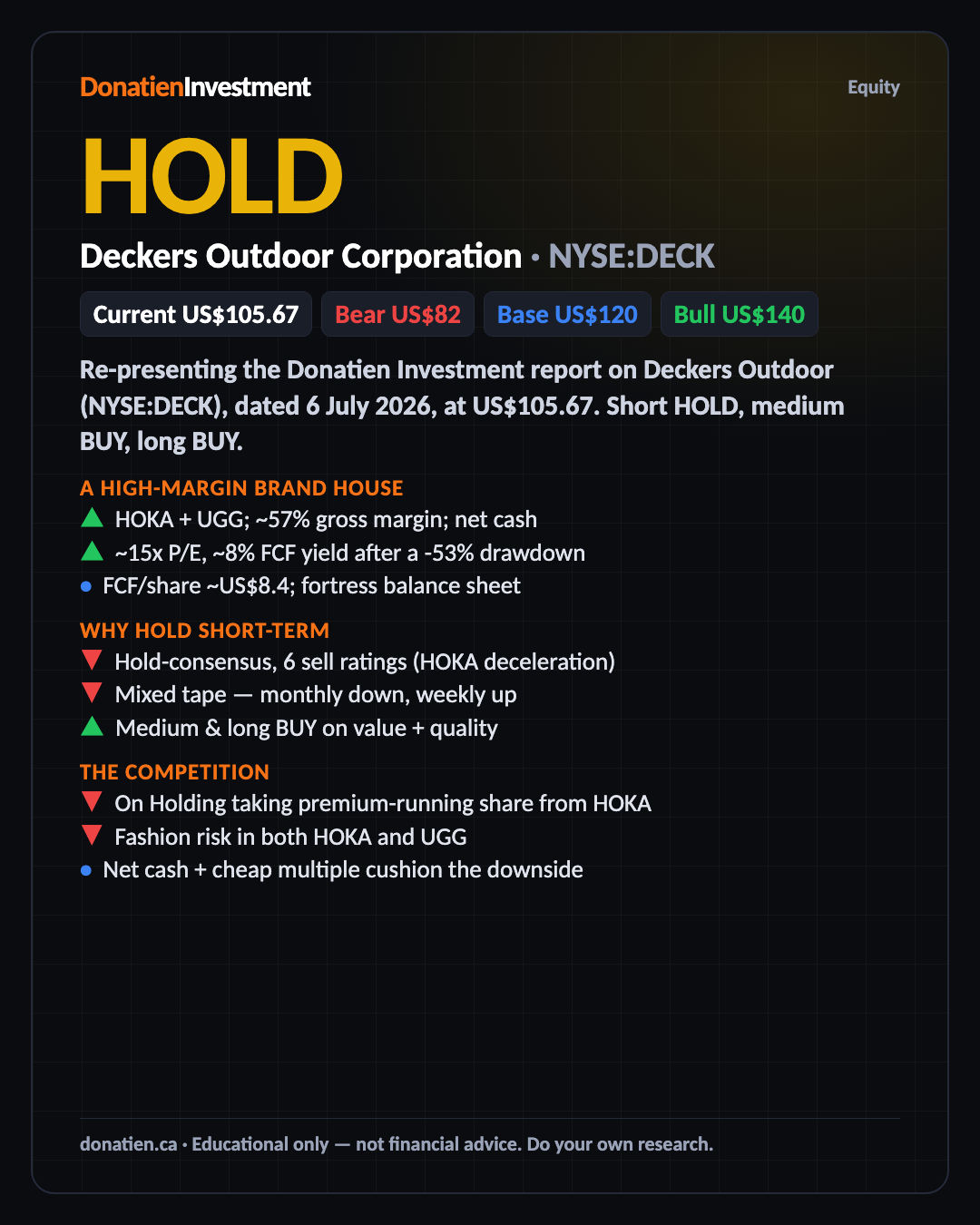

Deckers Outdoor Corporation (NYSE:DECK) HOLD

Deckers is a high-margin, net-cash brand house — HOKA and UGG — trading at about fifteen times earnings after a 53 per cent drawdown. But the Street is only hold-consensus, with six sell ratings on HOKA's deceleration, and the tape is mixed, so it's a hold short-term; medium and long term the value and quality rate a BUY.

Re-presenting the Donatien Investment report on Deckers Outdoor (NYSE:DECK), dated 6 July 2026, at US$105.67. Short HOLD, medium BUY, long BUY.

A high-margin brand house

Deckers is built around two powerhouse footwear brands: HOKA, in fast-growing performance running, and UGG, in premium comfort. It earns about fifty-seven per cent gross margins — elite for footwear — sits on a net-cash balance sheet, and converts profit into strong free cash flow. After a fifty-three per cent drawdown from its high, it trades at about fifteen times earnings with roughly an eight per cent free-cash-flow yield.

Why hold short-term

Two things hold it at a hold near-term. The Street is only hold-consensus, with six outright sell ratings, reflecting genuine worry about HOKA's growth decelerating and fashion risk in both brands. And the tape is mixed — the monthly trend is still down while the weekly is trying to turn up. The valuation and quality are attractive for the medium and long term, but the near-term picture is murky.

The competition

The main competitive vector is On Holding, which is taking share in premium running and directly challenging HOKA. Nike and Adidas are scale incumbents that can respond, and both Deckers brands are fashion-exposed — heat can fade. None of that breaks the thesis at a fifteen-times multiple and net cash, but it's why the short-term is a hold and any position is best scaled in.

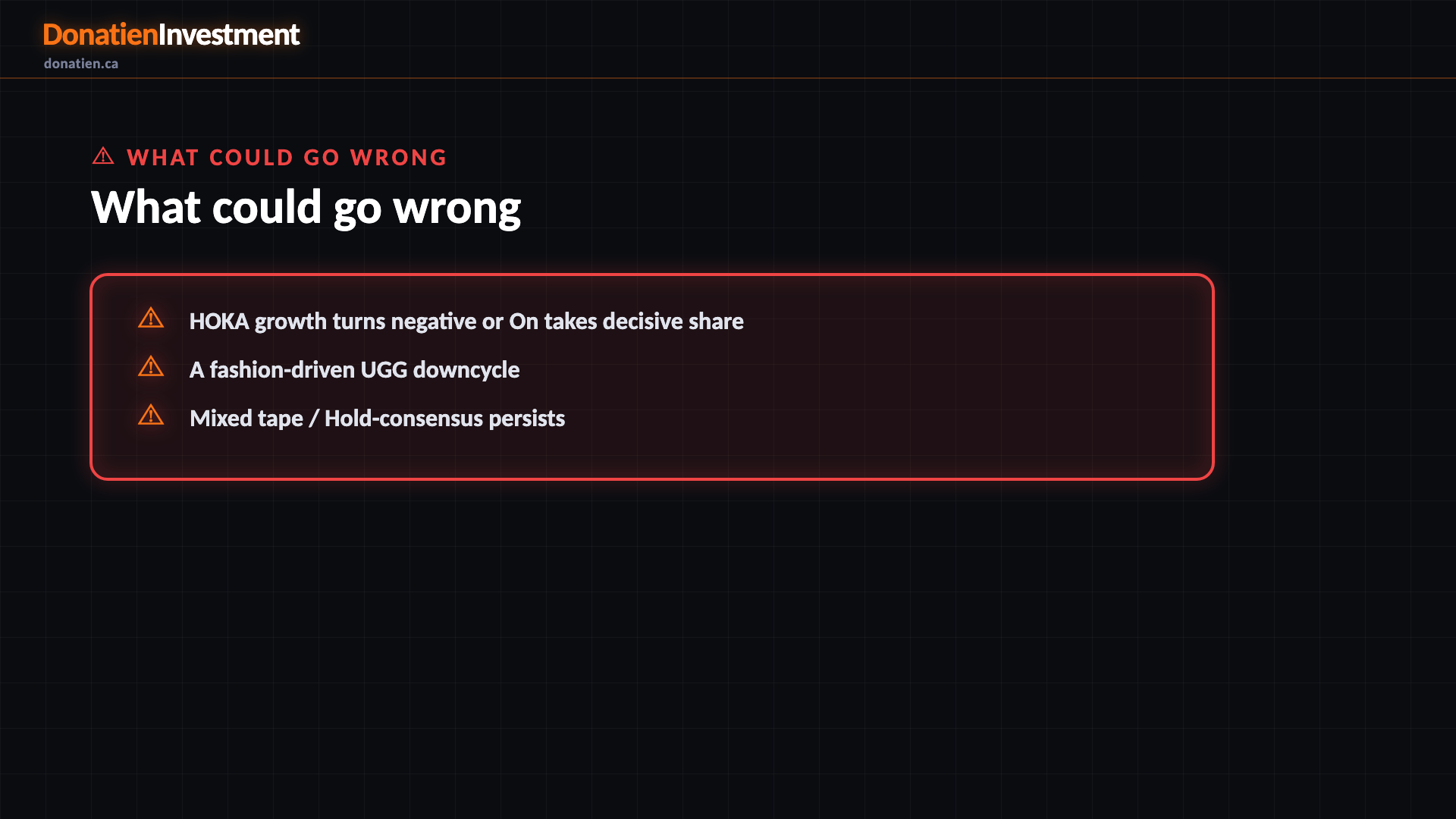

What could go wrong

HOKA growth turns negative or On takes decisive share. A fashion-driven UGG downcycle. Mixed tape / Hold-consensus persists.

Risk vs Reward

The report weights three twelve-month paths. The base case — most likely at 50 per cent — sees Deckers around US$120 on steady growth and net-cash buybacks, about 14 per cent above today. The bull at 25 per cent reaches US$140 if HOKA re-accelerates and the Street turns more positive. The bear at 25 per cent takes it to US$82 if HOKA decelerates further or On takes share — a fat competitive tail.

The verdict

The bottom line: a high-margin, net-cash brand house at about fifteen times earnings and an eight per cent free-cash-flow yield after a fifty-three per cent drawdown — attractive value for the medium and long term, which rate a BUY. But the Street is only hold-consensus with six sells on HOKA, and the tape is mixed, so near-term it's a hold. Scale in on a confirmed weekly turn or a clean earnings print, rather than chasing.

Read the full report on donatien.ca →{kind=link}

{kind=link}