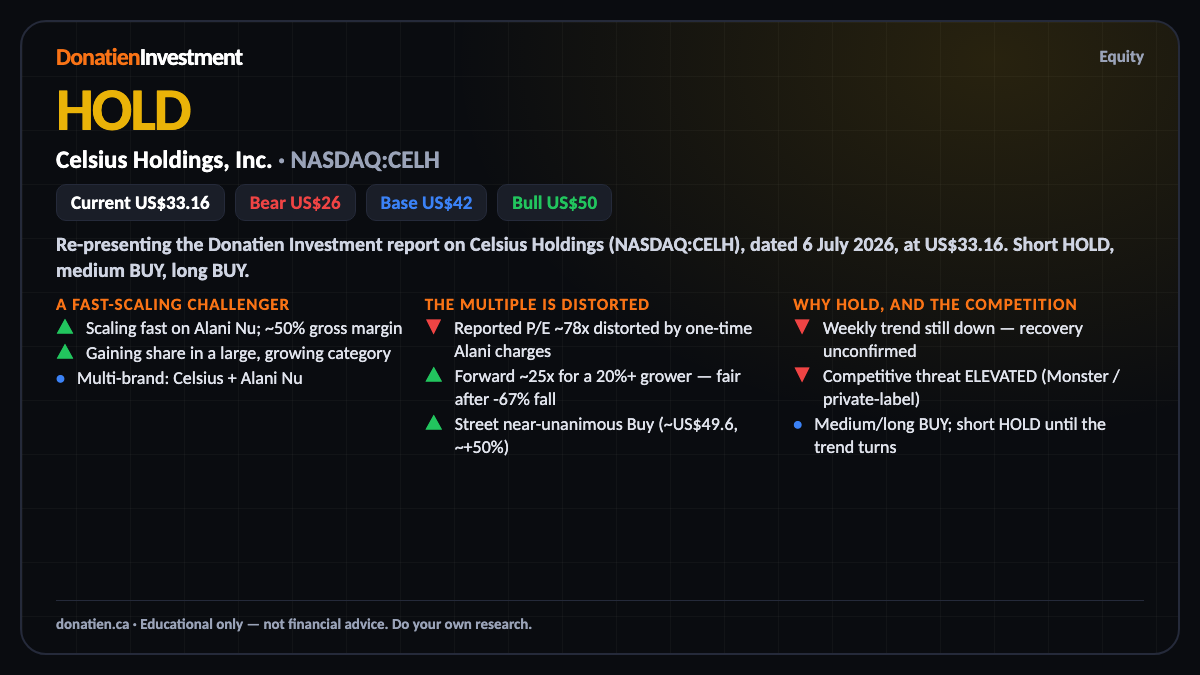

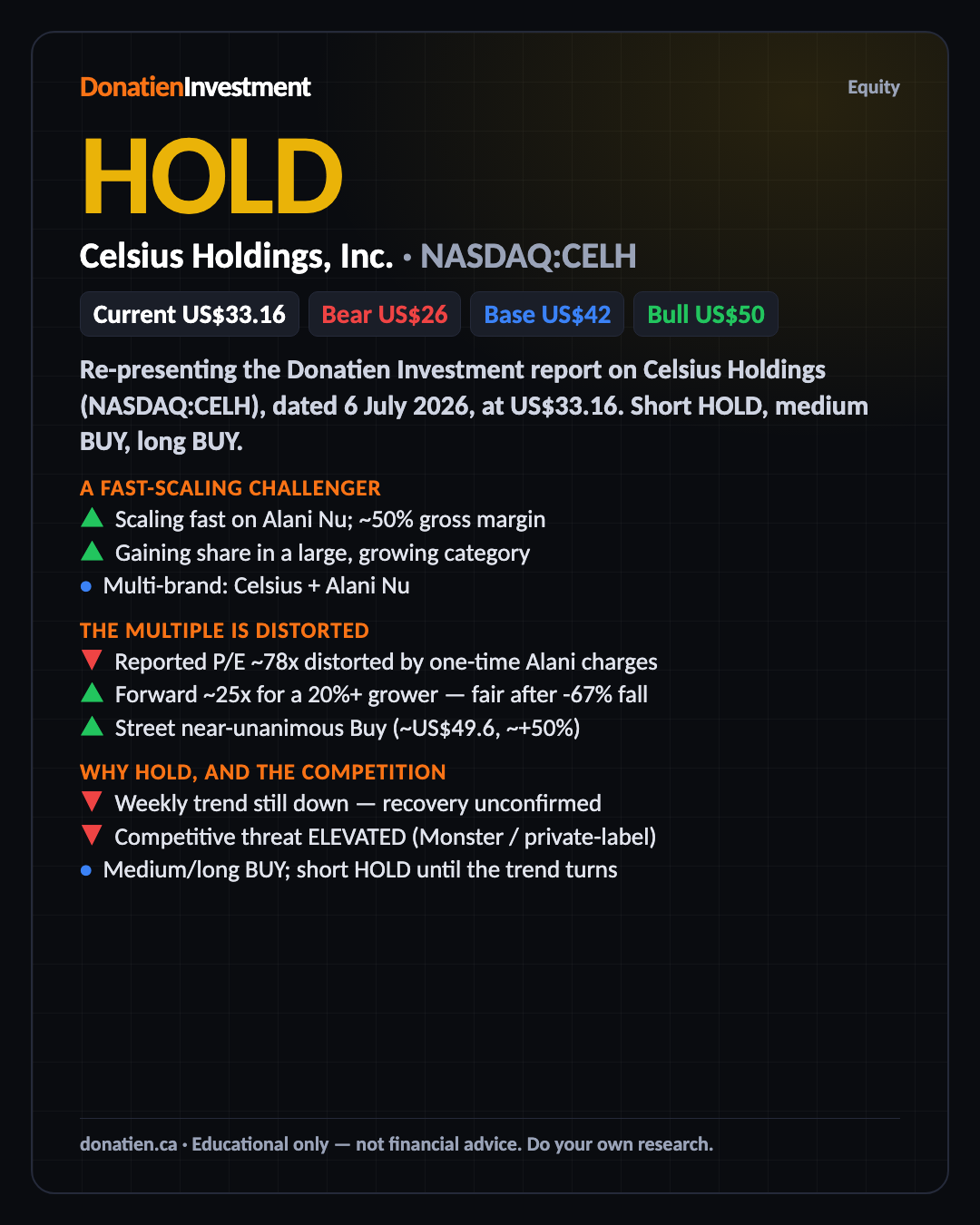

Celsius Holdings, Inc. (NASDAQ:CELH) HOLD

Celsius is a fast-scaling energy-drink challenger that has fallen sixty-seven per cent from its high. Its reported P/E looks extreme, but that's distorted by one-time Alani integration charges — on a forward basis it's about twenty-five times for a twenty-per-cent-plus grower, which is fair. The daily chart is recovering but the weekly trend hasn't confirmed, so it's a hold short-term; medium and long are BUY.

Re-presenting the Donatien Investment report on Celsius Holdings (NASDAQ:CELH), dated 6 July 2026, at US$33.16. Short HOLD, medium BUY, long BUY.

A fast-scaling challenger

Celsius makes functional energy drinks with a better-for-you, fitness positioning, distributed through Pepsi. After acquiring Alani Nu it is now a multi-brand platform that roughly doubled in scale and is taking share in a big, growing US energy-drink market. Gross margins are strong at about fifty per cent, and revenue is scaling fast. It is a genuine number-three-and-rising challenger to Monster and Red Bull.

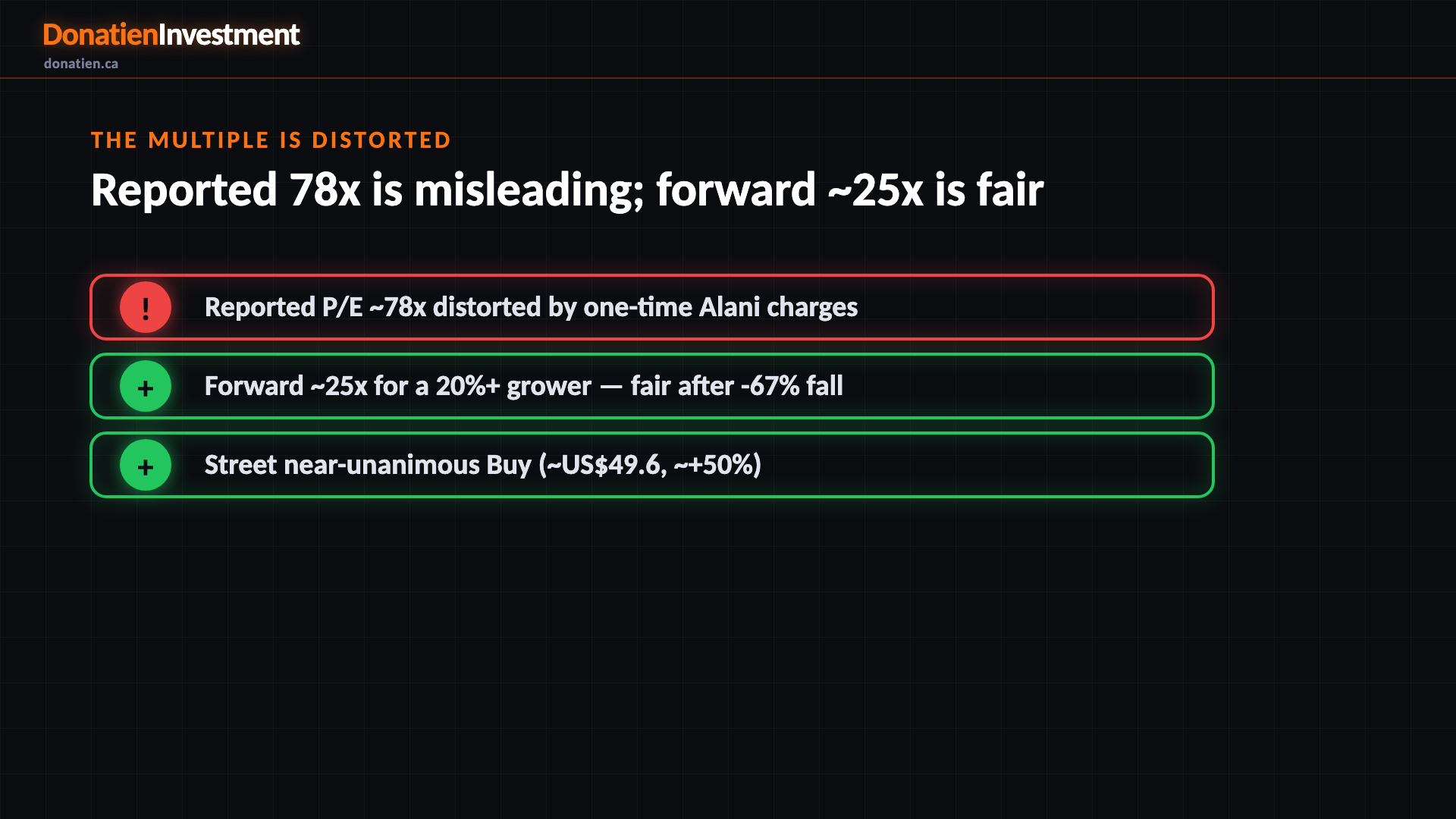

The multiple is distorted

On the screen the trailing P/E looks extreme, near eighty times — but that is misleading. A one-time operating loss last quarter, from Alani integration and inventory charges, depresses the trailing number. On a forward run-rate the multiple is about twenty-five times, which is fair for a twenty-per-cent-plus grower, especially after a sixty-seven per cent drawdown that has taken out most of the froth. The Street is near-unanimous buy with a target around fifty dollars.

Why hold, and the competition

Two things keep it a hold short-term. The daily chart has turned up off the twenty-eight dollar base, but the weekly trend is still down, so the recovery isn't confirmed. And the competitive threat is elevated — Monster, Red Bull and private-label crowd the category, and switching costs are low, so the share gains the multiple assumes have to keep coming. Medium and long term the risk-reward is a buy; near-term it is a hold until the trend confirms.

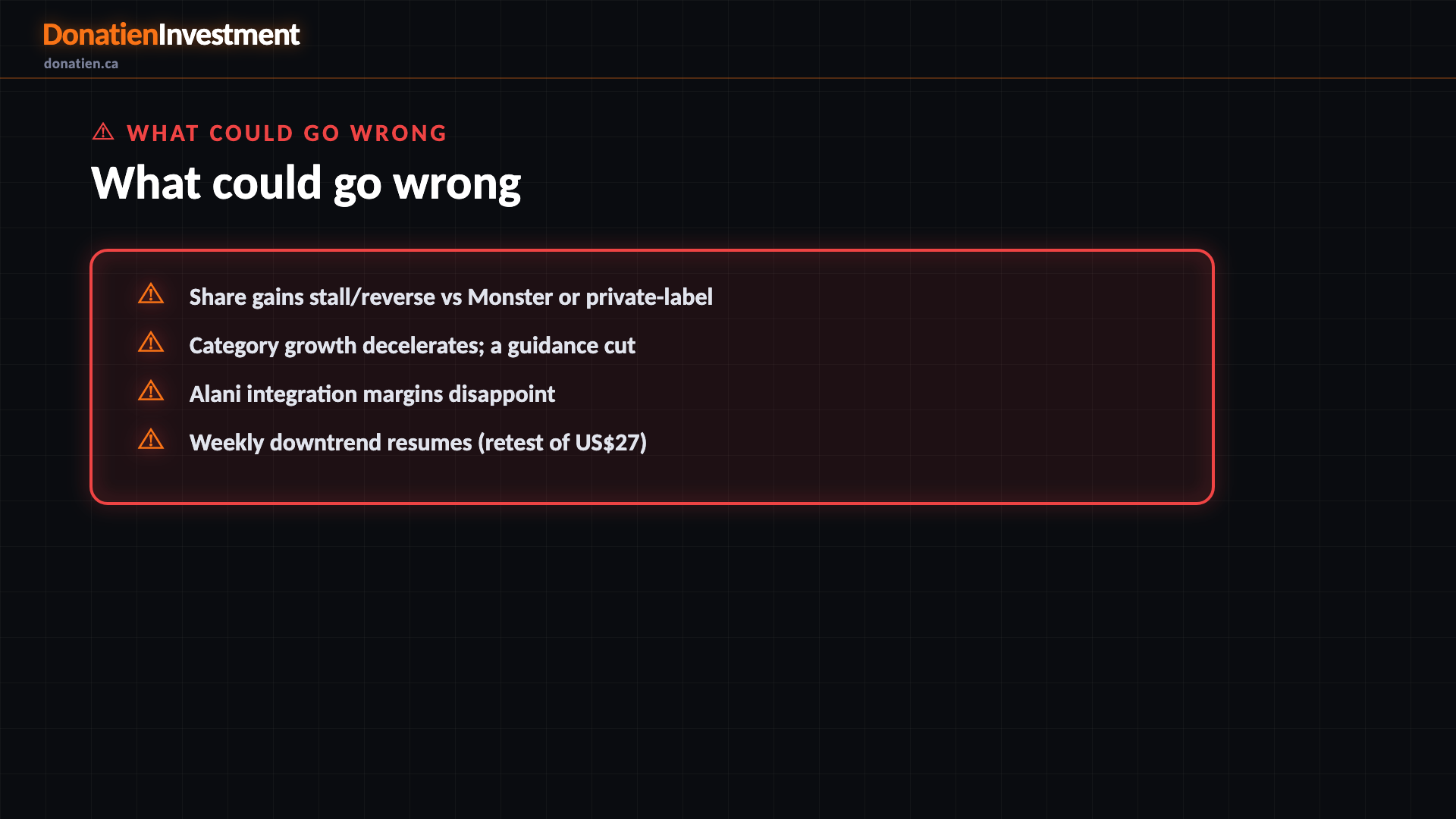

What could go wrong

Share gains stall/reverse vs Monster or private-label. Category growth decelerates; a guidance cut. Alani integration margins disappoint. Weekly downtrend resumes (retest of US$27).

Risk vs Reward

The report weights three twelve-month paths with a positive skew but a fat competitive tail. The base case — most likely at 50% — sees Celsius around US$42 as growth continues and margins recover, about twenty-seven per cent above today. The bull case (25%) reaches US$50 if Alani synergies land and share gains continue, toward the Street. The bear (25%) takes it to US$26 if Monster and private-label stall the share gains and margins disappoint — a retest of the lows.

The verdict

The bottom line: after a sixty-seven per cent fall, most of the froth is gone, and on a forward multiple this is a reasonably-priced, fast-scaling challenger with a near-unanimous-buy Street behind it. Medium and long term that earns a buy. But the weekly trend hasn't confirmed the turn and the competition is fierce, so near-term it is a hold — a Half-Size scale-in on the recovery, with a confirmed weekly turn or a clean quarter the trigger to add.

Read the full report on donatien.ca →{kind=link}

{kind=link}