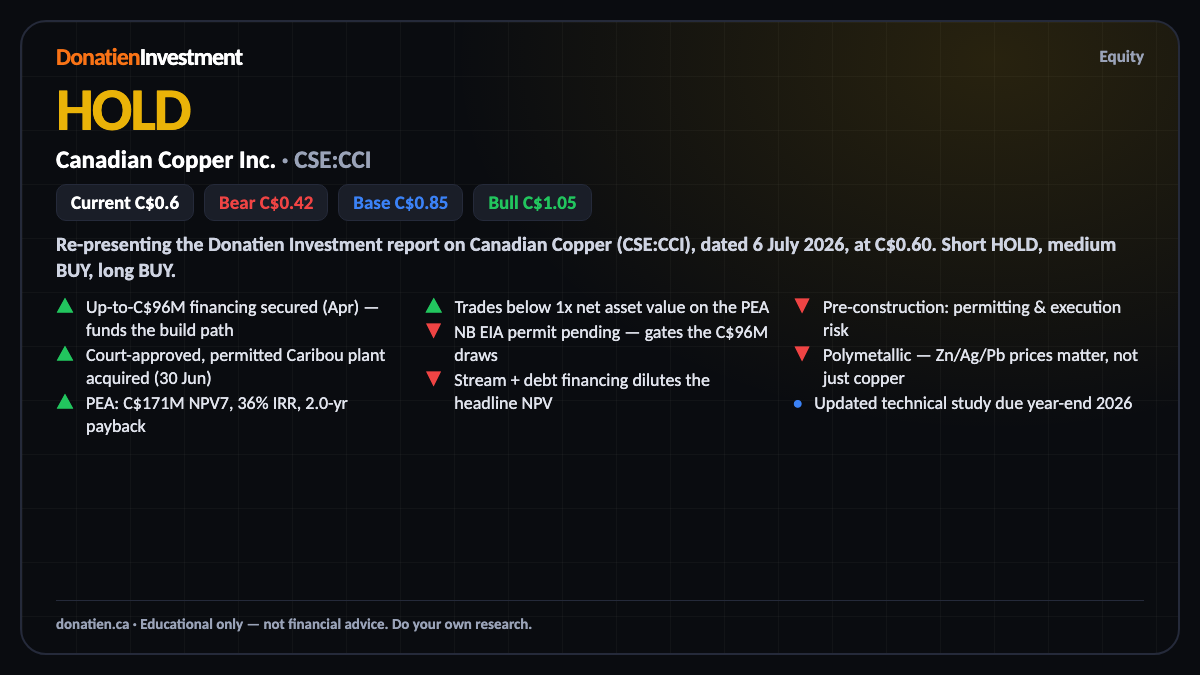

Canadian Copper Inc. (CSE:CCI) HOLD

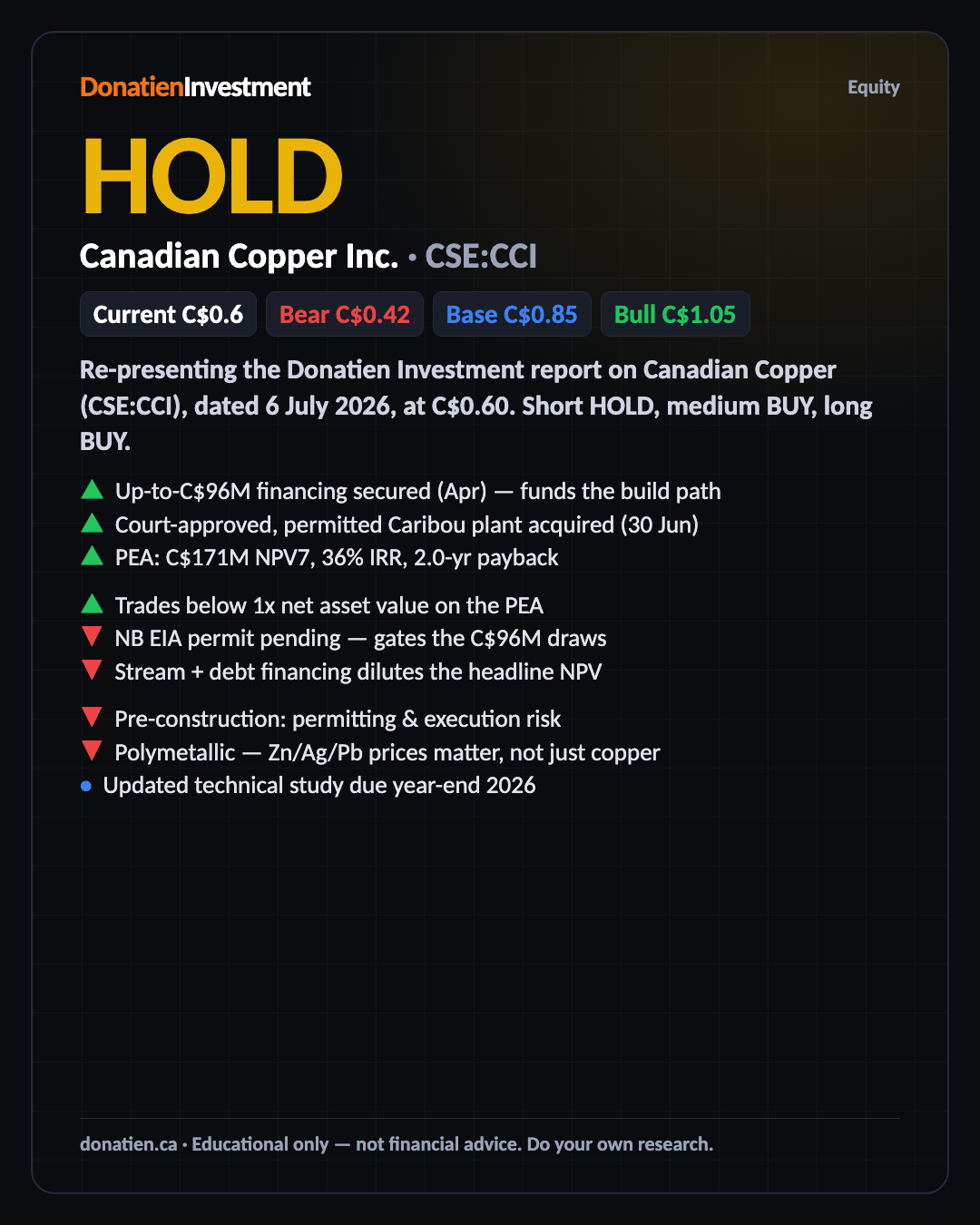

Canadian Copper has materially de-risked — an up-to-C$96M financing package and a court-approved, permitted brownfield plant, on a PEA showing a C$171M net present value and a 36% return, priced below one times net asset value. But copper is flat and the environmental permit that unlocks the construction draws is still pending, so it is a hold short-term; the medium- and long-term signals are BUY.

Re-presenting the Donatien Investment report on Canadian Copper (CSE:CCI), dated 6 July 2026, at C$0.60. Short HOLD, medium BUY, long BUY.

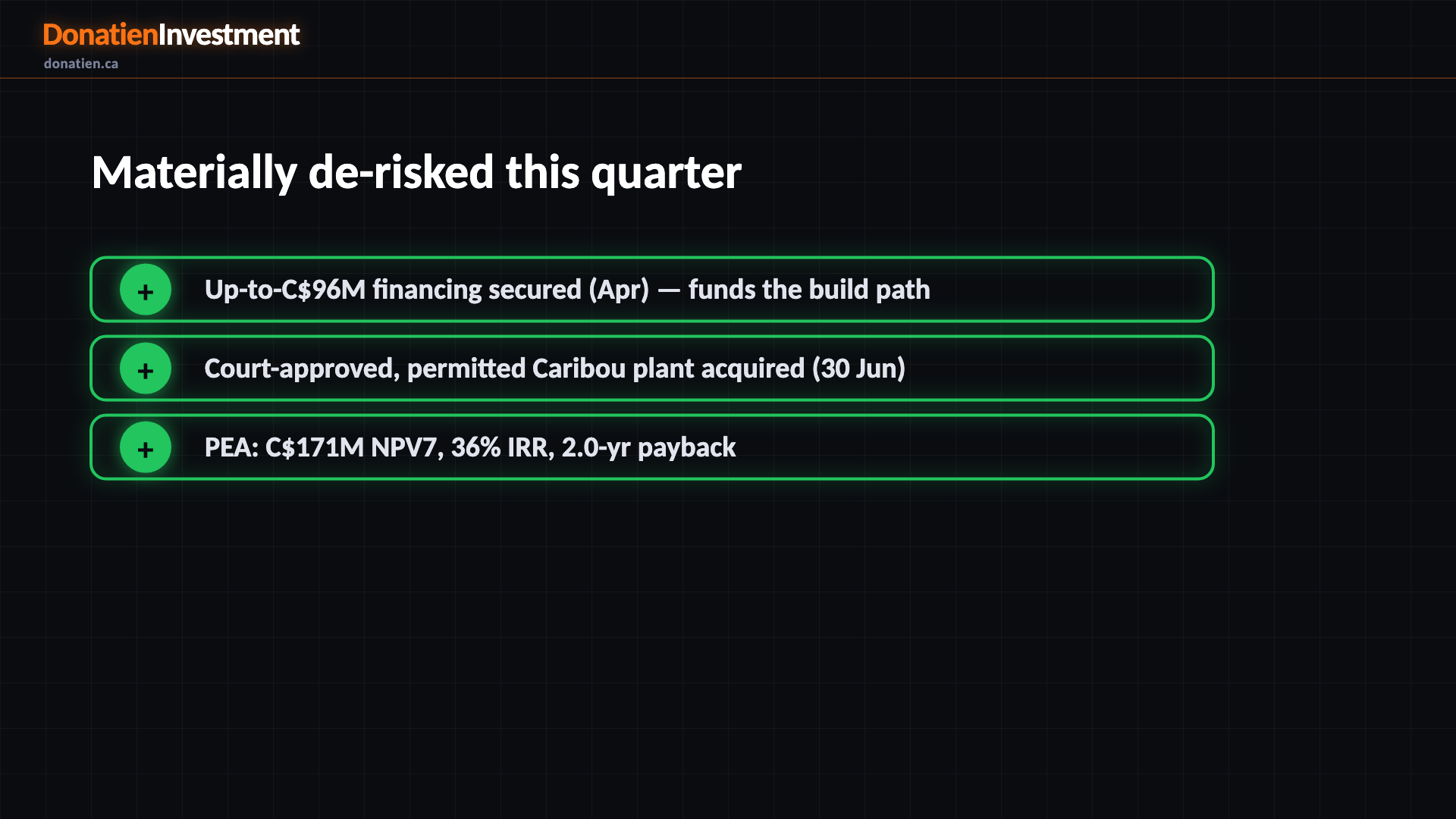

Materially de-risked this quarter

The story changed since our last look. Canadian Copper lined up an up-to-ninety-six-million-dollar financing package in April, and in late June won court approval to buy the permitted, recently-operated Caribou process plant near Bathurst. That brownfield plant is the whole thesis — it avoids the biggest cost and permitting hurdle a new mill would face. On top of that sits a preliminary economic study showing a hundred-and-seventy-one-million-dollar net present value, a thirty-six per cent return, and a two-year payback.

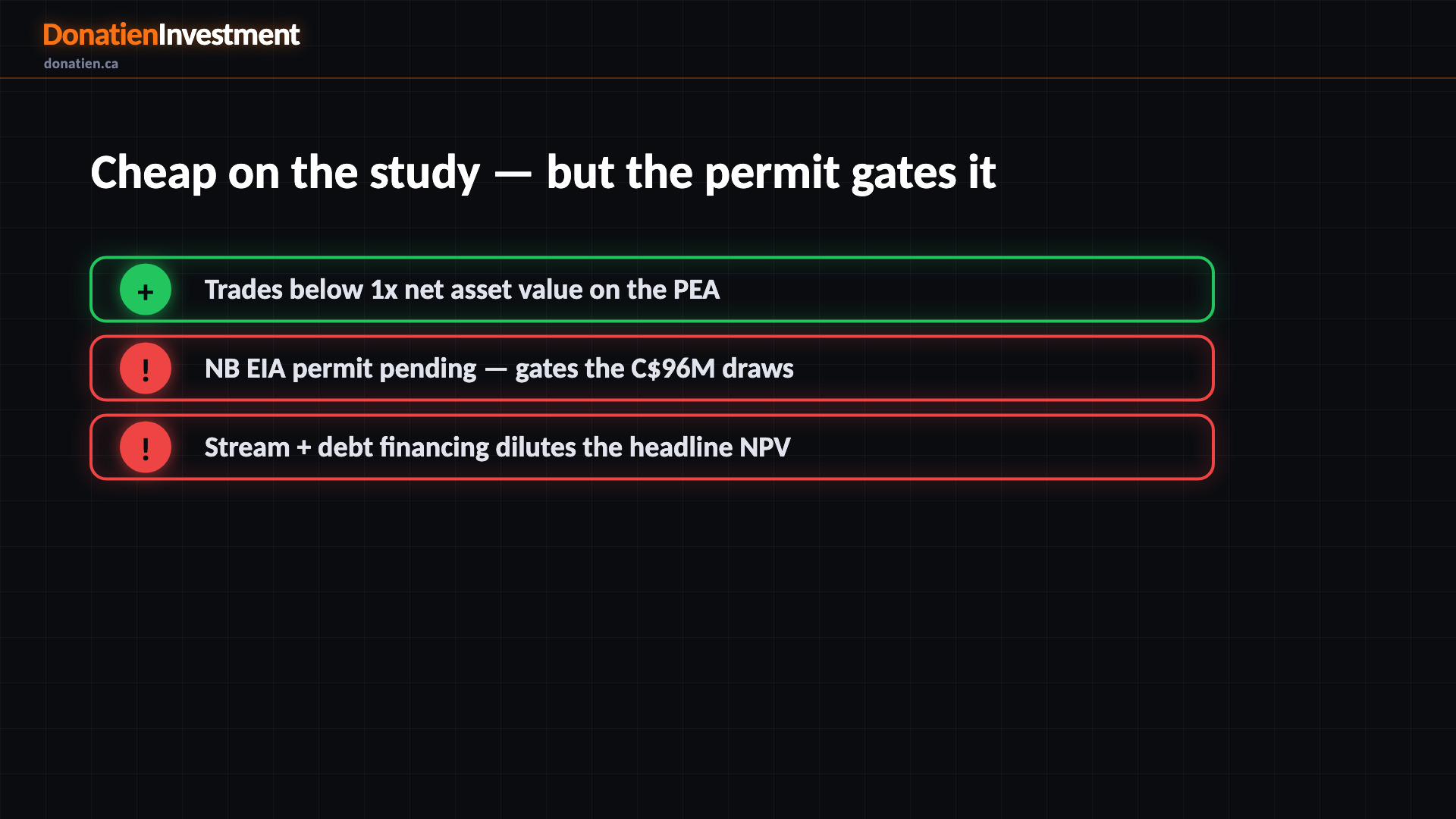

Cheap on the study — but the permit gates it

At a hundred-and-fifteen-million-dollar market value against a hundred-and-seventy-one-million net present value, the shares trade below one times net asset value — genuinely cheap for a financed developer. The catch, and the reason it is a hold rather than a buy today, is that the construction draws are conditional on the New Brunswick environmental permit, which is not yet granted. Copper is also flat and the deposit is really a polymetallic mix, so silver and zinc matter as much as copper.

A polymetallic developer with real risks

This remains a pre-construction developer, so execution and permitting are the swing risks. The financing stack — a precious-metals stream plus debt at a high spread — leaks value the headline study does not capture, and further dilution is likely. It is copper in name, but the value is spread across zinc, silver and lead, so a base-metals selloff hits it directly. None of that breaks the thesis; it is why the near-term call is a hold and any position is best scaled in.

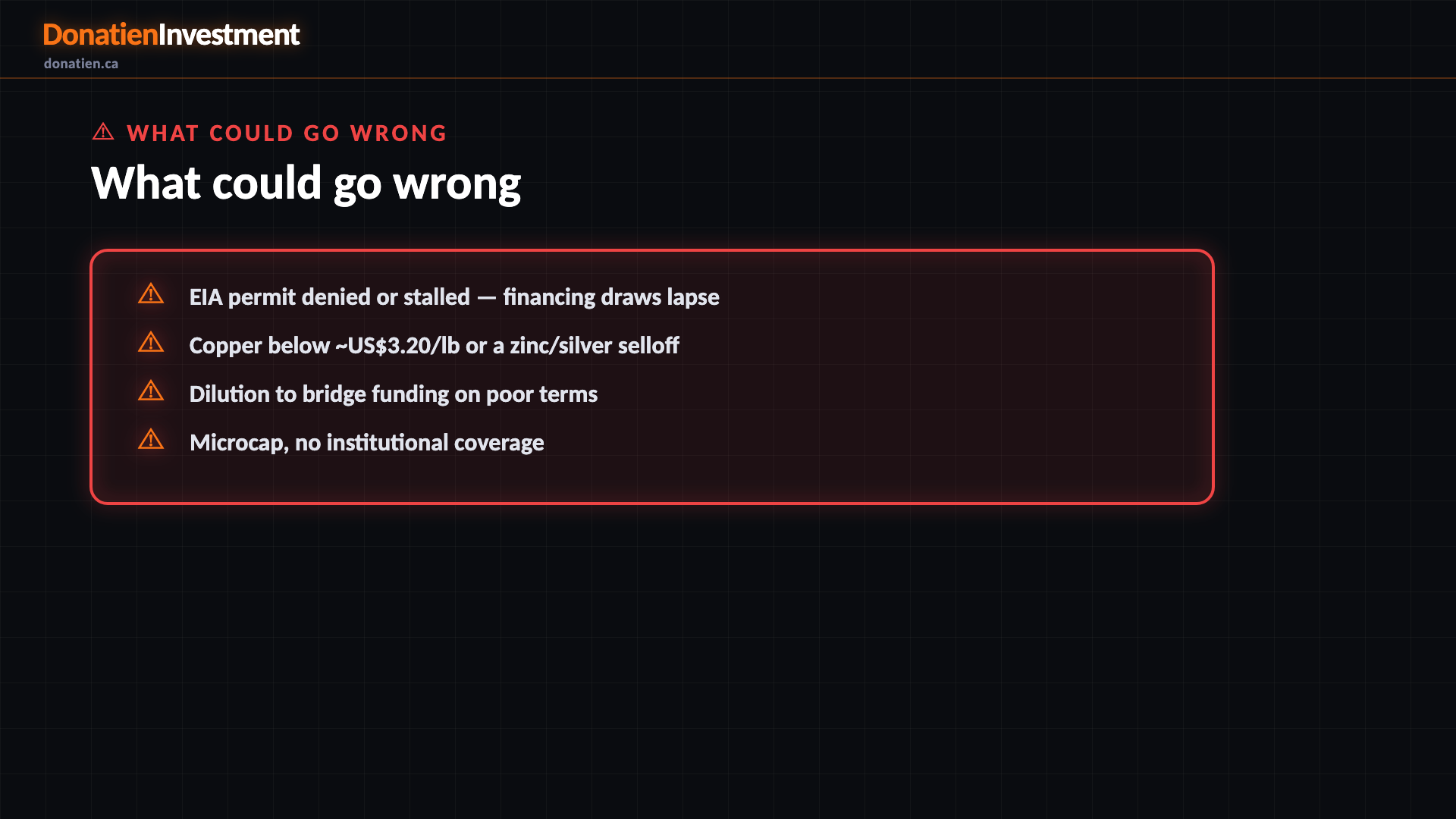

What could go wrong

EIA permit denied or stalled — financing draws lapse. Copper below ~US$3.20/lb or a zinc/silver selloff. Dilution to bridge funding on poor terms. Microcap, no institutional coverage.

Risk vs Reward

The report weights three twelve-month paths. The base case — most likely at 55% — puts Canadian Copper around C$0.85 (about +42%) as permitting advances and drilling adds ounces. The bull case (25%) reaches C$1.05 if the EIA permit lands, the construction draws flow and copper firms. The bear (20%) takes it to C$0.42 if the permit stalls and base metals weaken. A sub-1x-NAV, financed project with a permit-gated re-rate — hence a hold now, a buy for the medium and long term.

The verdict

The bottom line: Canadian Copper has secured funding and a permitted brownfield plant on a project that screens cheap below net asset value, which earns a medium- and long-term buy. But the environmental permit that releases the construction money is still pending, so the near-term call is a hold. A confirmed permit step, or a firm hold of C$0.54, is the trigger to lean in.

Read the full report on donatien.ca →{kind=link}

{kind=link}