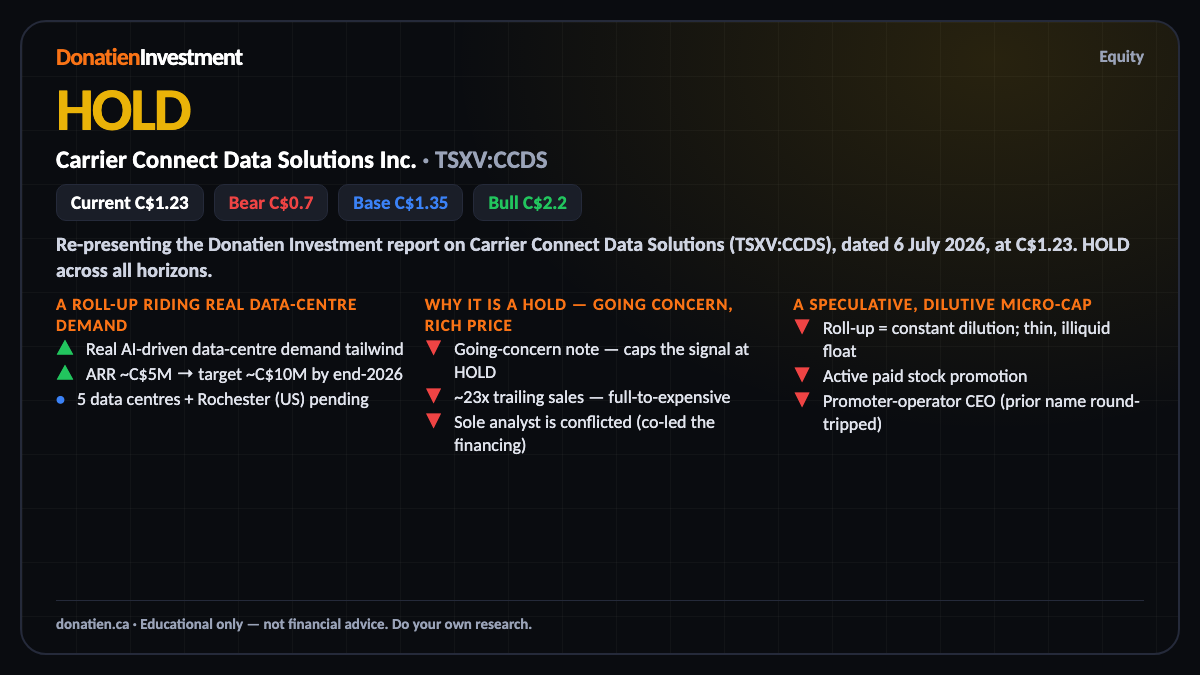

Carrier Connect Data Solutions Inc. (TSXV:CCDS) HOLD

Carrier Connect is a data-centre colocation roll-up riding genuine AI-driven demand — but its audited accounts carry a going-concern note that caps it at hold, it is richly priced at about 23 times trailing sales, thinly traded, and led by a serial promoter. A speculative hold, with the entry ladder at wait.

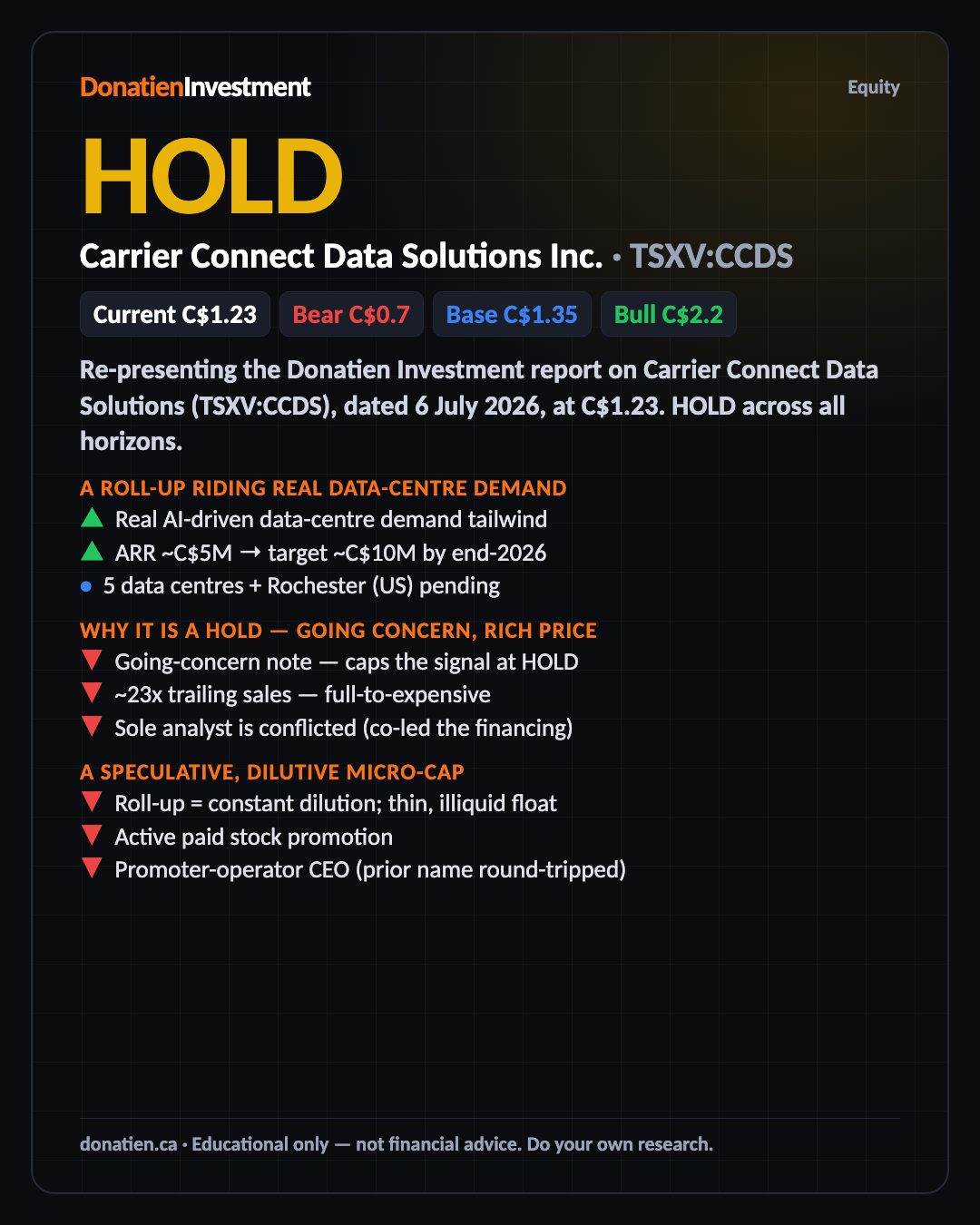

Re-presenting the Donatien Investment report on Carrier Connect Data Solutions (TSXV:CCDS), dated 6 July 2026, at C$1.23. HOLD across all horizons.

A roll-up riding real data-centre demand

The idea is straightforward. Carrier Connect buys small, underused colocation data centres, fills the empty racks, and consolidates them into a public portfolio — betting that private sites bought at two-to-three times revenue re-rate to ten times or more as a public company. The demand backdrop is real: AI compute is driving data-centre needs hard. It runs five sites with a sixth pending, and recurring revenue is around five million dollars, targeted to roughly double by year-end.

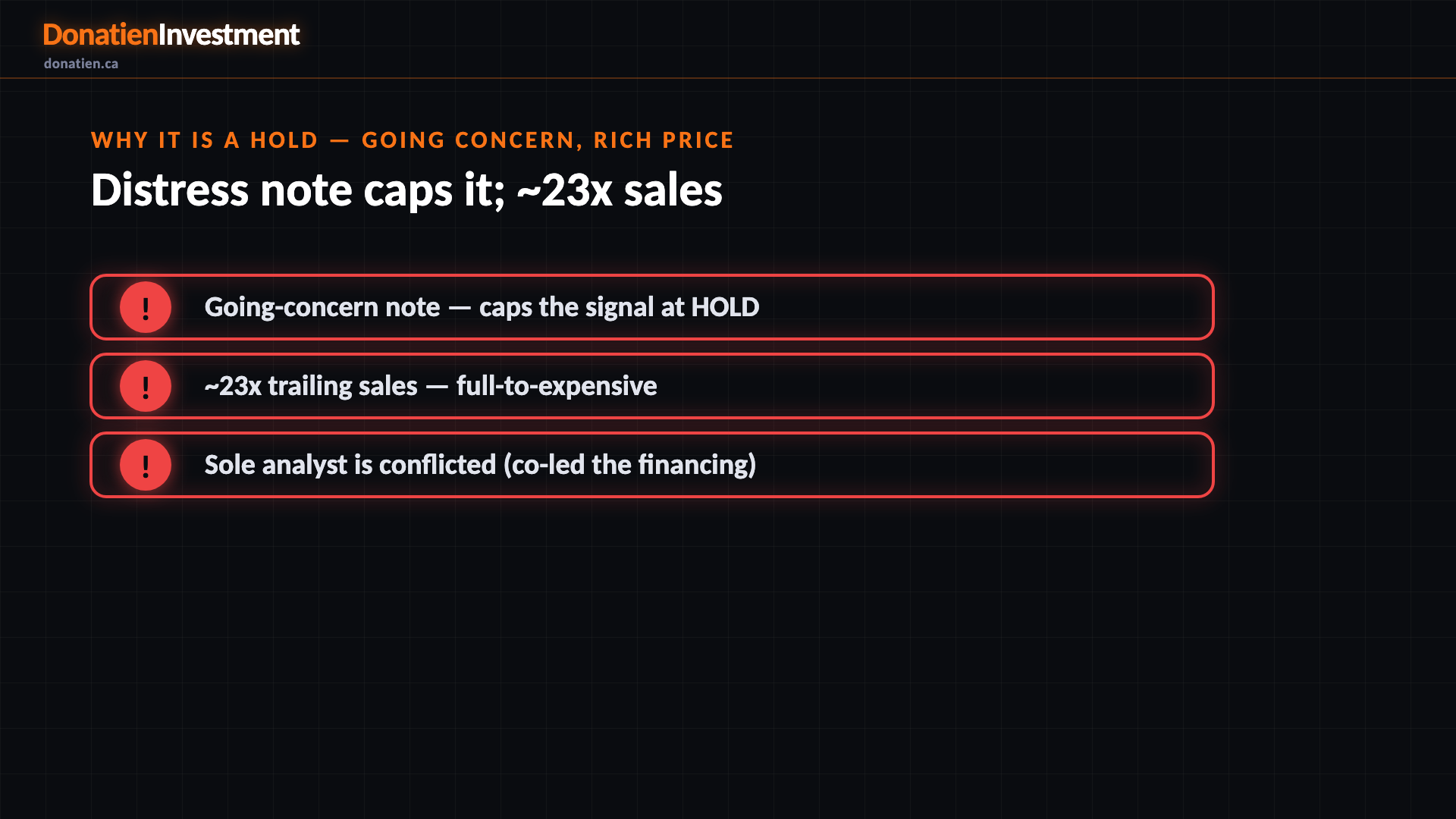

Why it is a hold — going concern, rich price

Here is what caps it. The audited financials carry an explicit going-concern note — the company is still loss-making, with a trailing net loss over three million dollars — and that fires a financial-distress gate that holds the signal at hold no matter how good the demand story is. On top of that it trades around twenty-three times trailing sales, a full-to-expensive multiple that leans on recurring revenue it has not yet earned. The lone analyst backing it also co-led its financing, so treat that target with caution.

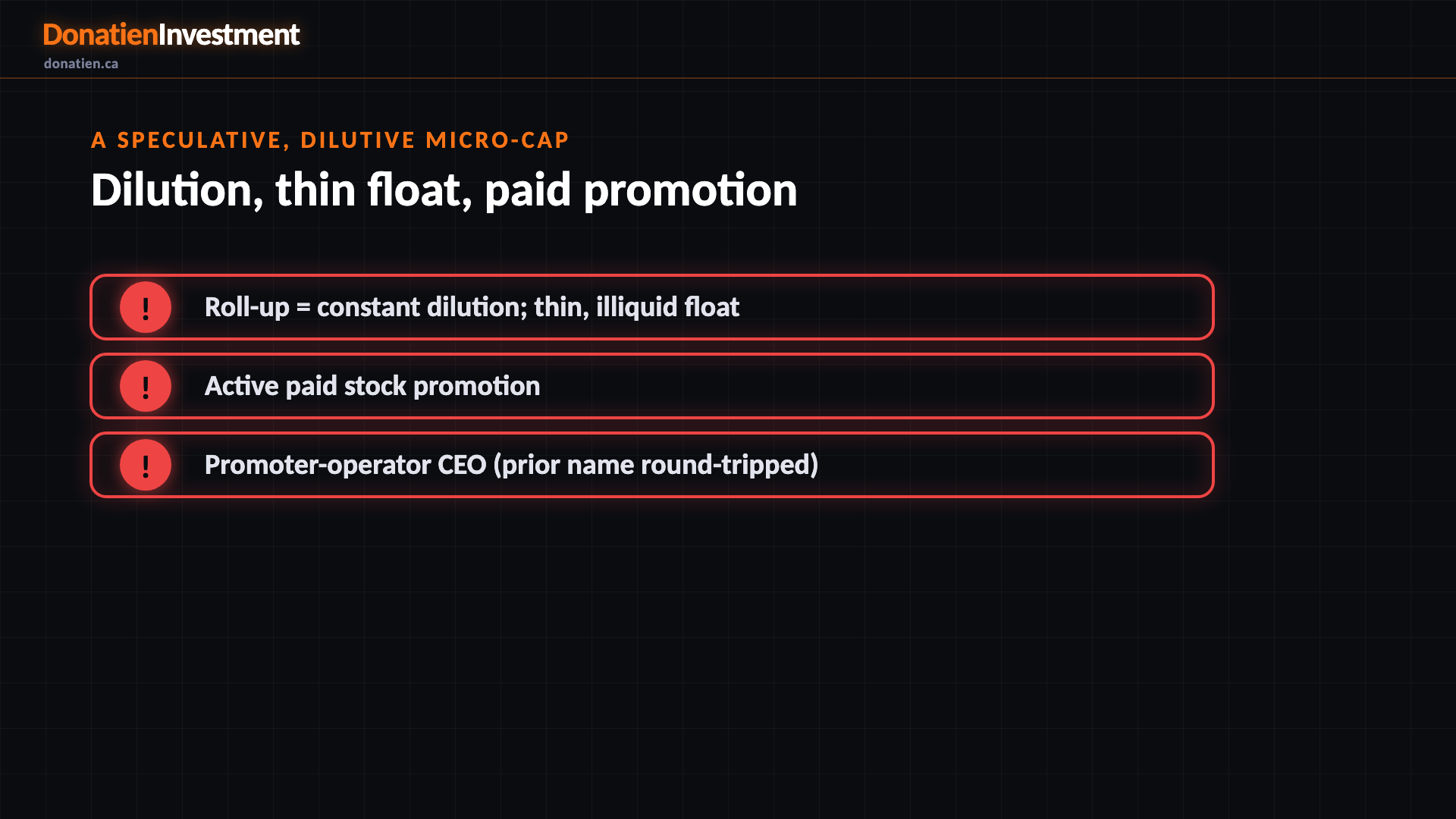

A speculative, dilutive micro-cap

This is high-variance. A roll-up funds itself by issuing shares, so dilution is constant, and the float is thin — only tens of thousands of shares trade a day, so exiting any size is hard. There is active paid stock promotion, and the chief executive's headline credential is a crypto-cycle re-rating that round-tripped. None of that is disqualifying, but it is why the honest call is a speculative hold with the entry ladder at wait, and any position kept small.

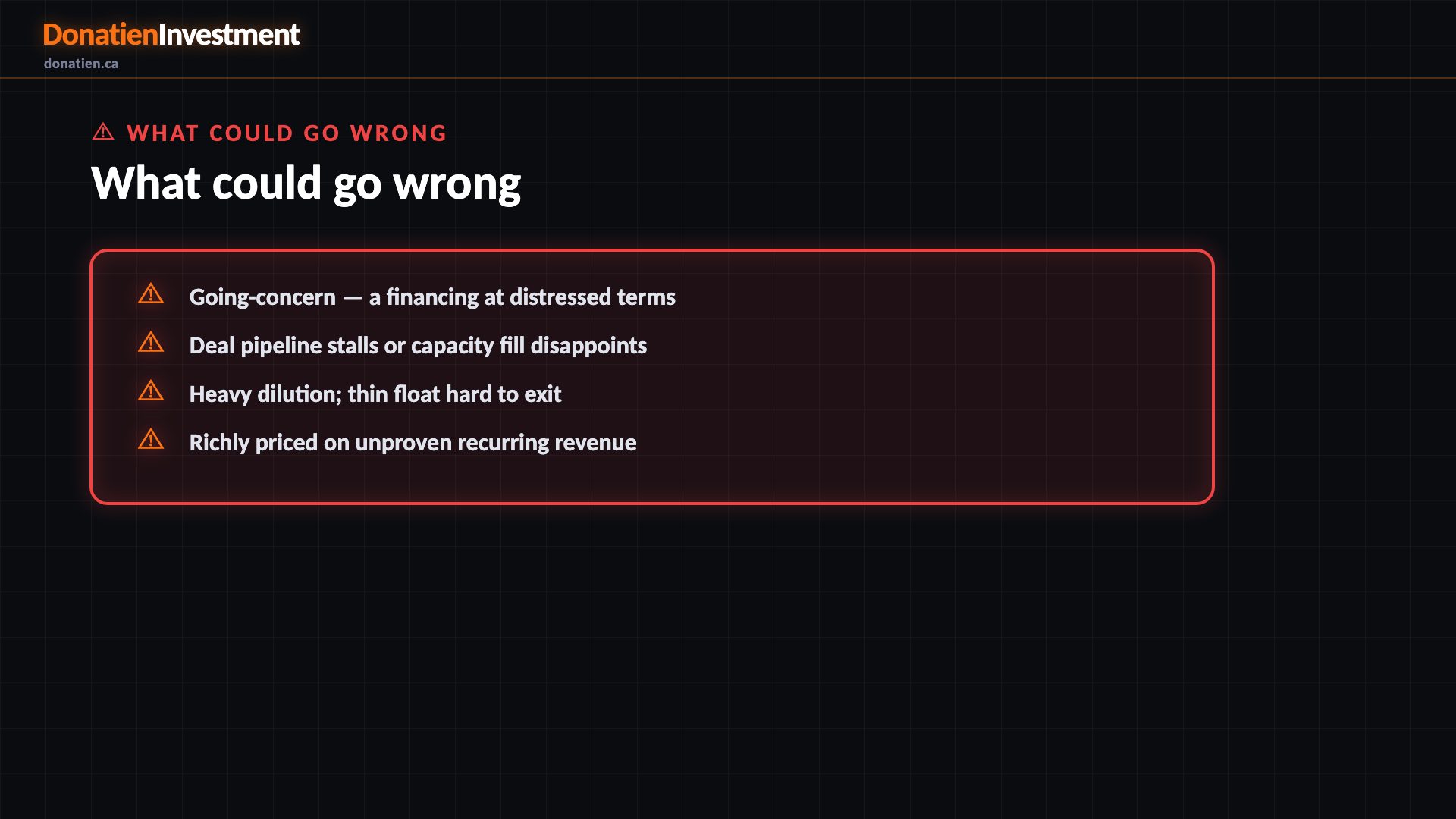

What could go wrong

Going-concern — a financing at distressed terms. Deal pipeline stalls or capacity fill disappoints. Heavy dilution; thin float hard to exit. Richly priced on unproven recurring revenue.

Risk vs Reward

The report weights three twelve-month paths, and the distribution is wide and financing-dependent. The base case — most likely at 50% — puts it around C$1.35 as recurring revenue grows but dilution and cash burn cap the re-rate; that barely clears today's price. The bull case (25%) reaches C$2.20 if acquisitions keep closing accretively, recurring revenue hits the ten-million target, and the multiple re-rates. The bear (25%) takes it to C$0.70 if the going-concern bites and a financing prints at distressed terms.

The verdict

The bottom line: the AI data-centre demand is real and the roll-up idea is coherent, but a going-concern note, a rich sales multiple, a thin float and active paid promotion are too much to underwrite as a buy. It is a speculative hold — for existing holders, keep it small and watch for a clean acquisition close and evidence of self-funding; it is not a name to chase.

Read the full report on donatien.ca →{kind=link}

{kind=link}