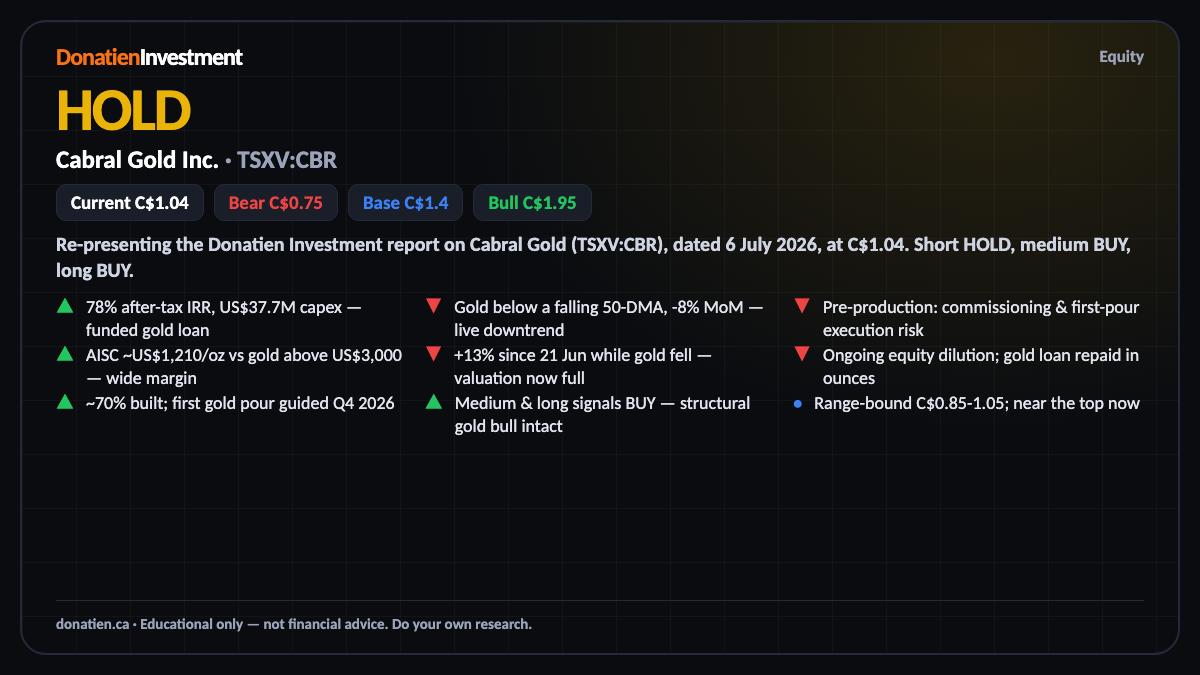

Cabral Gold Inc. (TSXV:CBR) HOLD

Cabral Gold is a funded, high-IRR gold developer about to pour its first gold — but gold is in a live short-term downtrend and a 13% run has richened the valuation into the full band, so it is a hold at C$1.04. The medium- and long-term signals are BUY, so the read is: accumulate on weakness, don't chase the top of the range.

Re-presenting the Donatien Investment report on Cabral Gold (TSXV:CBR), dated 6 July 2026, at C$1.04. Short HOLD, medium BUY, long BUY.

The starter mine is funded and high-margin

Cabral's appeal is a small heap-leach starter with exceptional economics for its size — a seventy-eight per cent after-tax return in the study, on under thirty-eight million US dollars of capital, at an all-in cost near twelve hundred dollars an ounce against a gold price above three thousand. Crucially it is fully funded by a gold loan with no attached share dilution, and construction is about seventy per cent done, with first gold guided for the fourth quarter. That funded, near-production status is the strength of the story.

Gold's downtrend caps it, and the price has run

Two things hold this at a hold today. Gold is in a live short-term downtrend — spot sits below a falling fifty-day average and is down about eight per cent on the month — which strips out the short-term tailwind a producer normally leans on. And the shares have run thirteen per cent since our last look while gold fell, pushing the value of the funded starter into what we would call the full band on a net-asset basis. The longer-term case is intact and rates a buy; the near-term entry is simply less generous than it was.

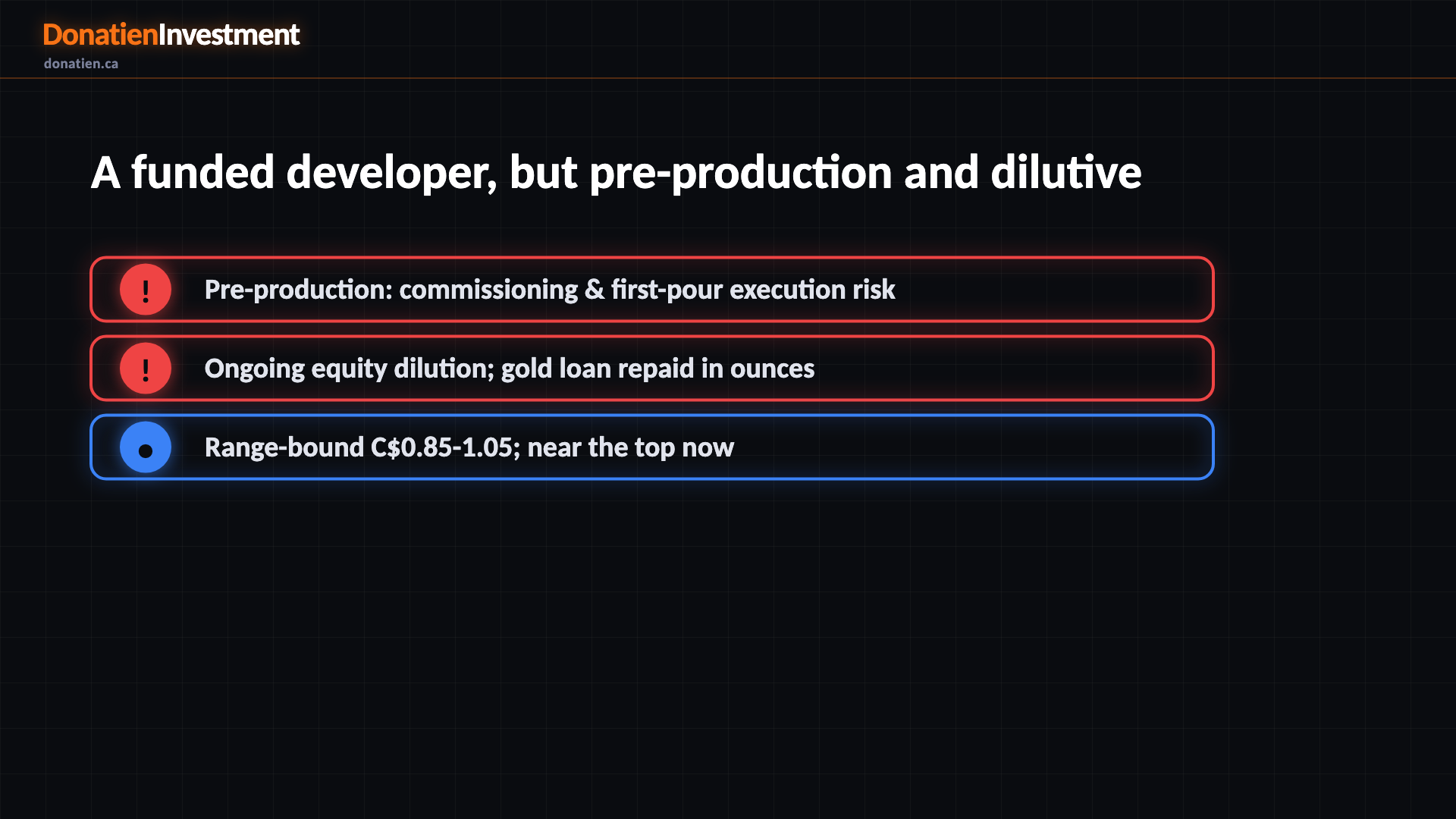

A funded developer, but pre-production and dilutive

This is still a single-asset, pre-revenue developer building its first mine, so execution through commissioning and the first pour is the swing risk. Exploration is funded by issuing shares, so dilution is ongoing, and the gold loan is repaid in ounces — a partial short position on the metal itself. None of that breaks the thesis, but it is why the near-term signal is a hold rather than a buy, and why a position is best built on weakness rather than chased at the top of the range.

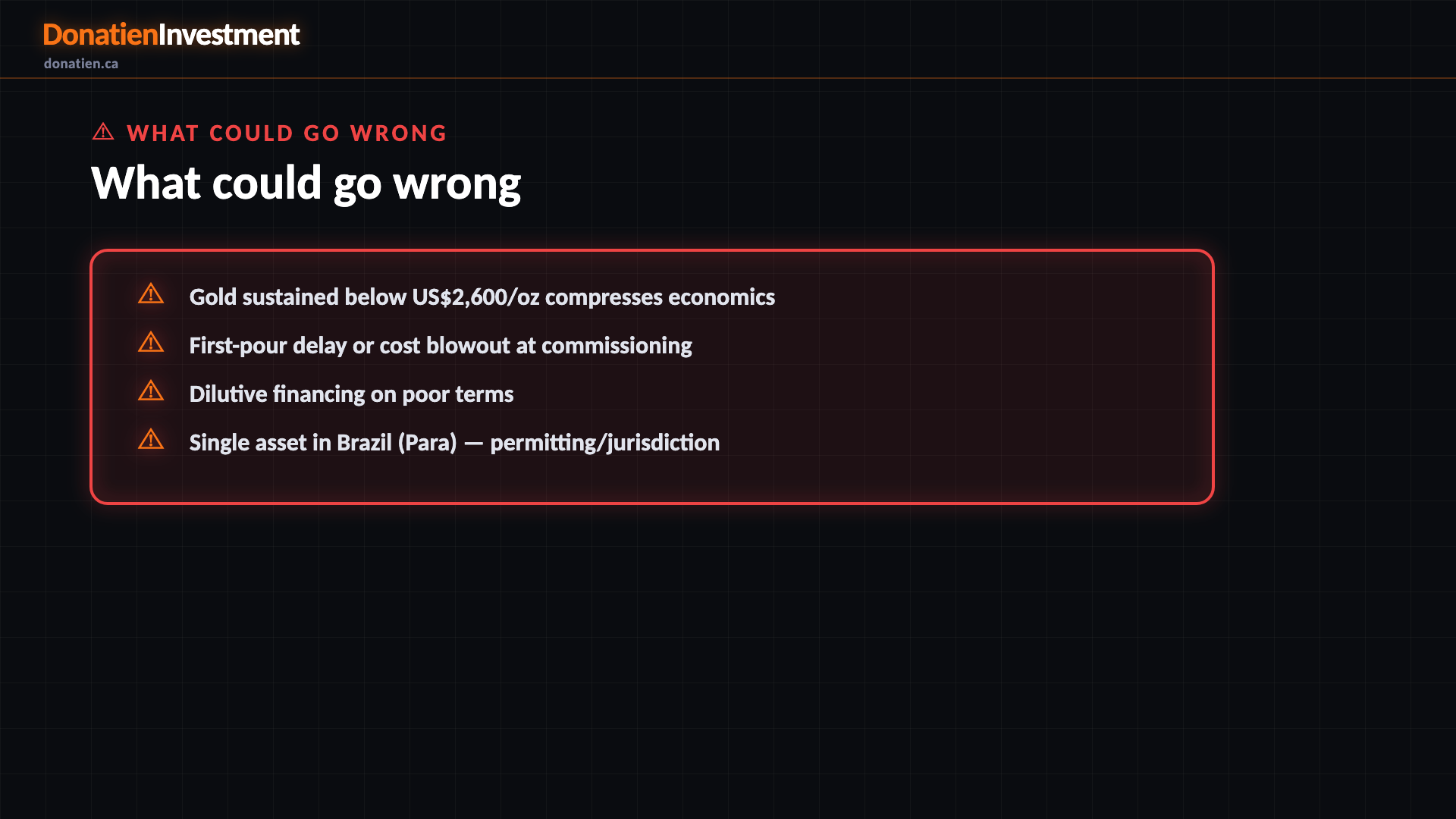

What could go wrong

Gold sustained below US$2,600/oz compresses economics. First-pour delay or cost blowout at commissioning. Dilutive financing on poor terms. Single asset in Brazil (Para) — permitting/jurisdiction.

Risk vs Reward

The report weights three twelve-month paths. The base case — the most likely at 55% — sees Cabral around C$1.40 as commissioning de-risks and gold holds its range, roughly a third above today. The bull case (25%) reaches C$1.95 on a clean first pour and firmer gold. The bear (20%) takes it to C$0.75 if gold breaks lower or the pour slips. The skew is positive over time, which is why the medium- and long-term calls are BUY — but the near-term entry is a hold, not a chase.

The verdict

The bottom line: Cabral is doing the hard part well — funding and building a high-return starter mine — and the medium- and long-term case is a buy. But at C$1.04, into a falling gold price and a full valuation, the near-term edge is gone. Hold here and accumulate on weakness toward the C$0.90 area or on a clean first gold pour, rather than chasing the top of the range.

Read the full report on donatien.ca →{kind=link}

{kind=link}