Booking Holdings Inc. (NASDAQ:BKNG) BUY

Booking is a dominant, capital-light travel platform trading at about nineteen times clean earnings — below what its quality warrants — with a six per cent free-cash-flow yield and a shrinking share count. The daily chart has just turned up on strong volume, so two of our three entry paths are met. A high-conviction BUY.

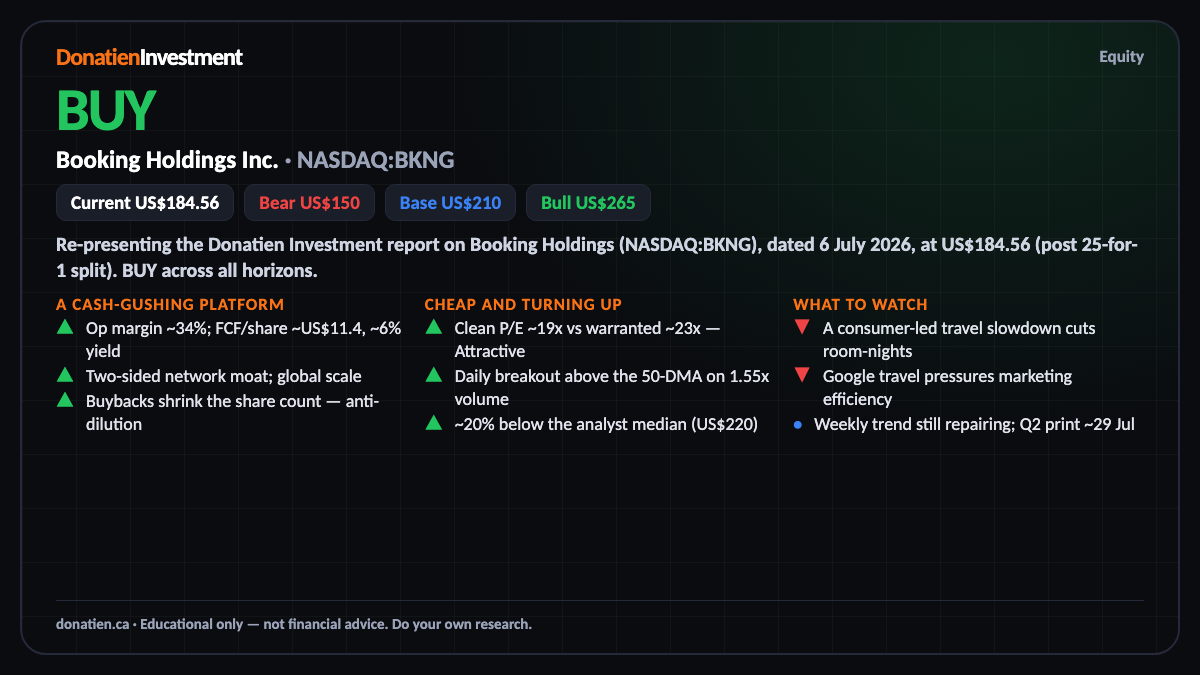

Re-presenting the Donatien Investment report on Booking Holdings (NASDAQ:BKNG), dated 6 July 2026, at US$184.56 (post 25-for-1 split). BUY across all horizons.

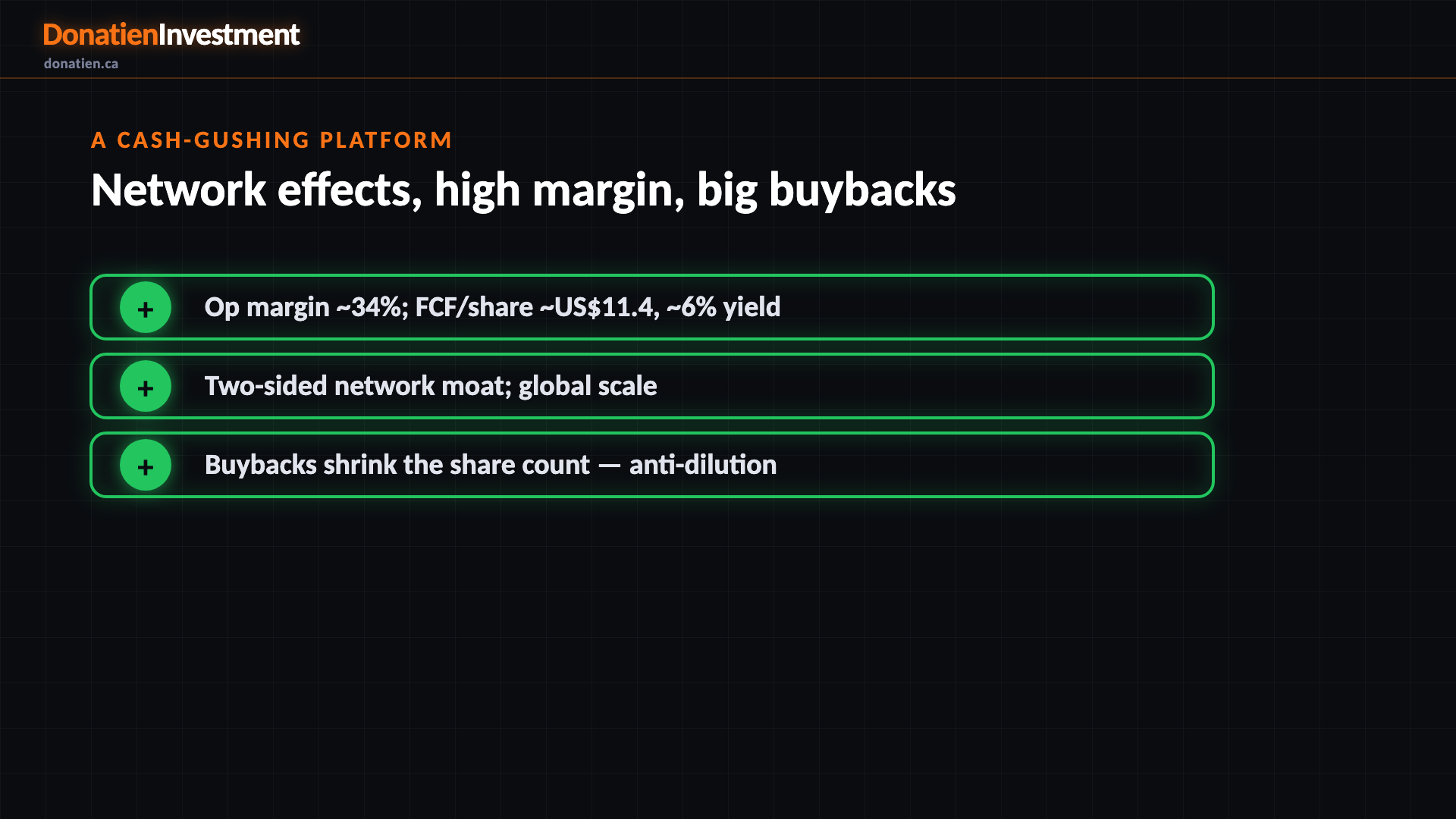

A cash-gushing platform

Booking is the world's largest online travel company, taking a commission on an enormous volume of travel through Booking-dot-com, Priceline and Agoda. It is capital-light and high-margin — a thirty-four per cent operating margin — and it converts almost all of its profit into free cash flow, most of which it returns through buybacks that shrink the share count. A powerful two-sided network — more properties attract more travellers and vice-versa — is the moat.

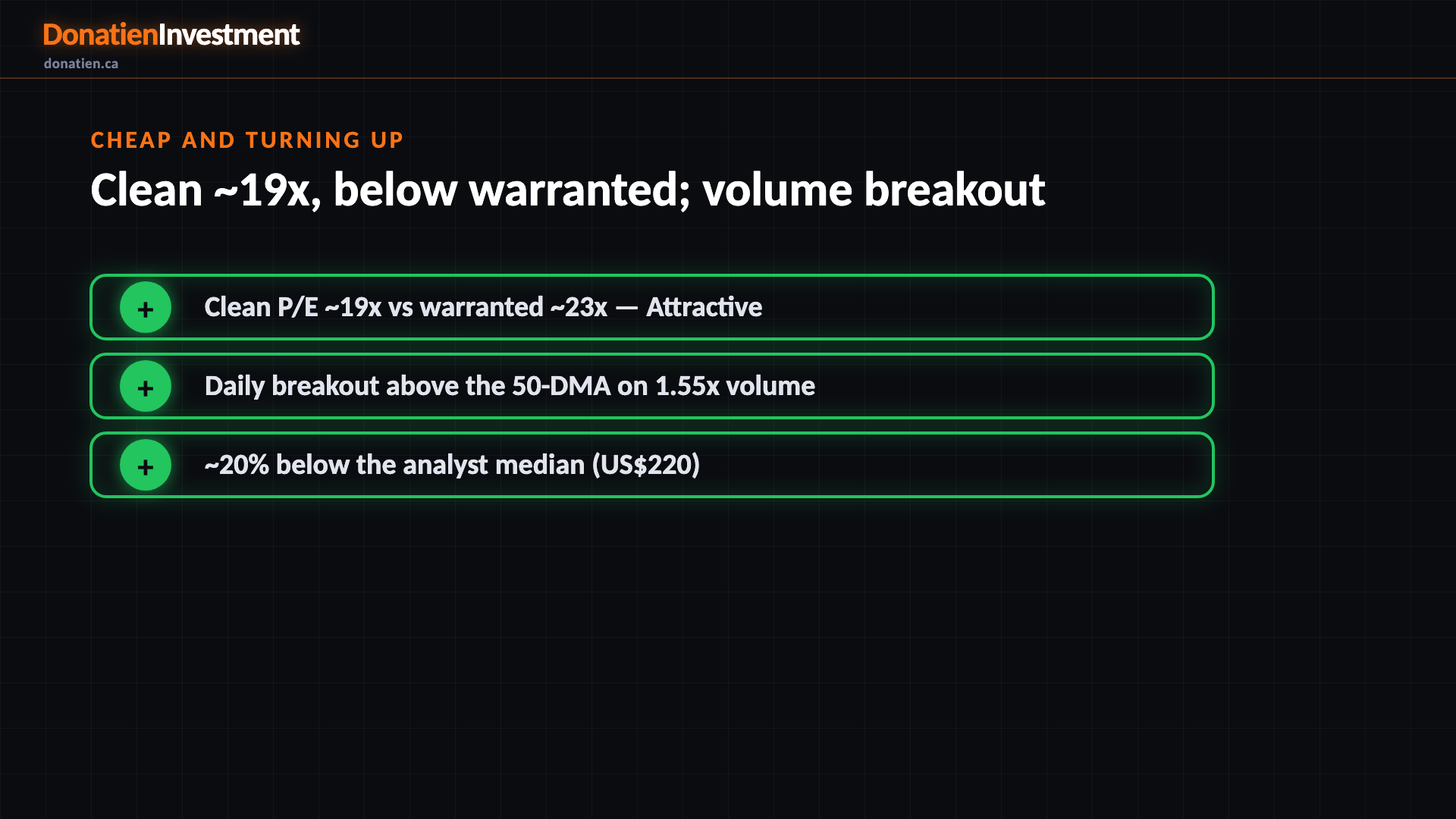

Cheap and turning up

On clean earnings Booking trades around nineteen times, below the twenty-three we'd warrant from rates and durable growth, and about twenty per cent under the analyst median. Unusually, its reported earnings understate operating power because non-operating items are a drag — a favourable distortion. And the timing has improved: the daily chart broke above its fifty-day average on one-and-a-half times normal volume, so both the value and the technical entry paths are met.

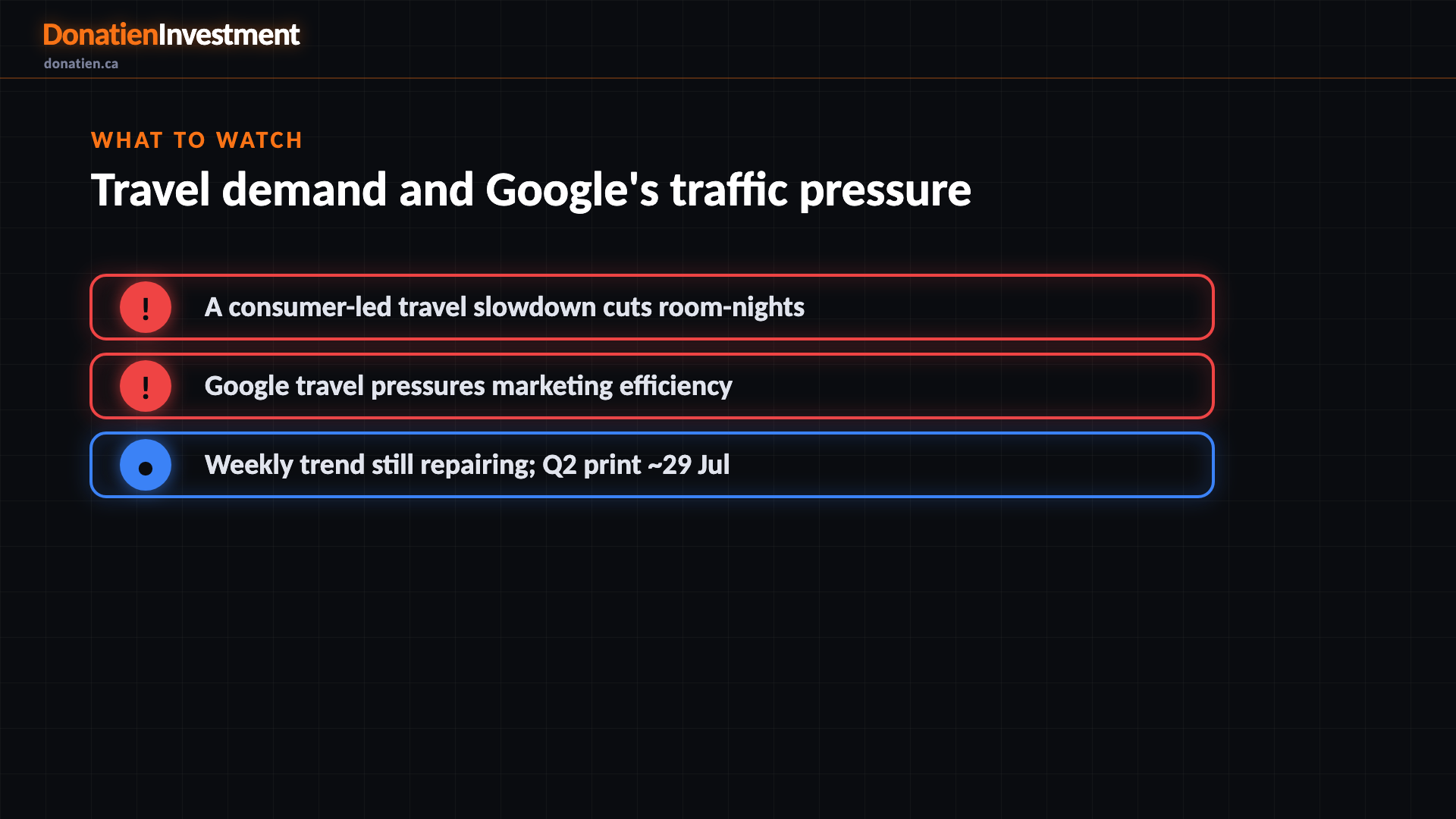

What to watch

The risks are real but manageable. A consumer-led travel slowdown would cut room-nights, and the weekly trend is still repairing, so this is early-innings rather than a fully-confirmed uptrend. The structural watch-item is Google — its travel meta-search pressures Booking's marketing efficiency, which is the key cost line. Neither breaks the thesis today, but a Q2 print at the end of July is the next test.

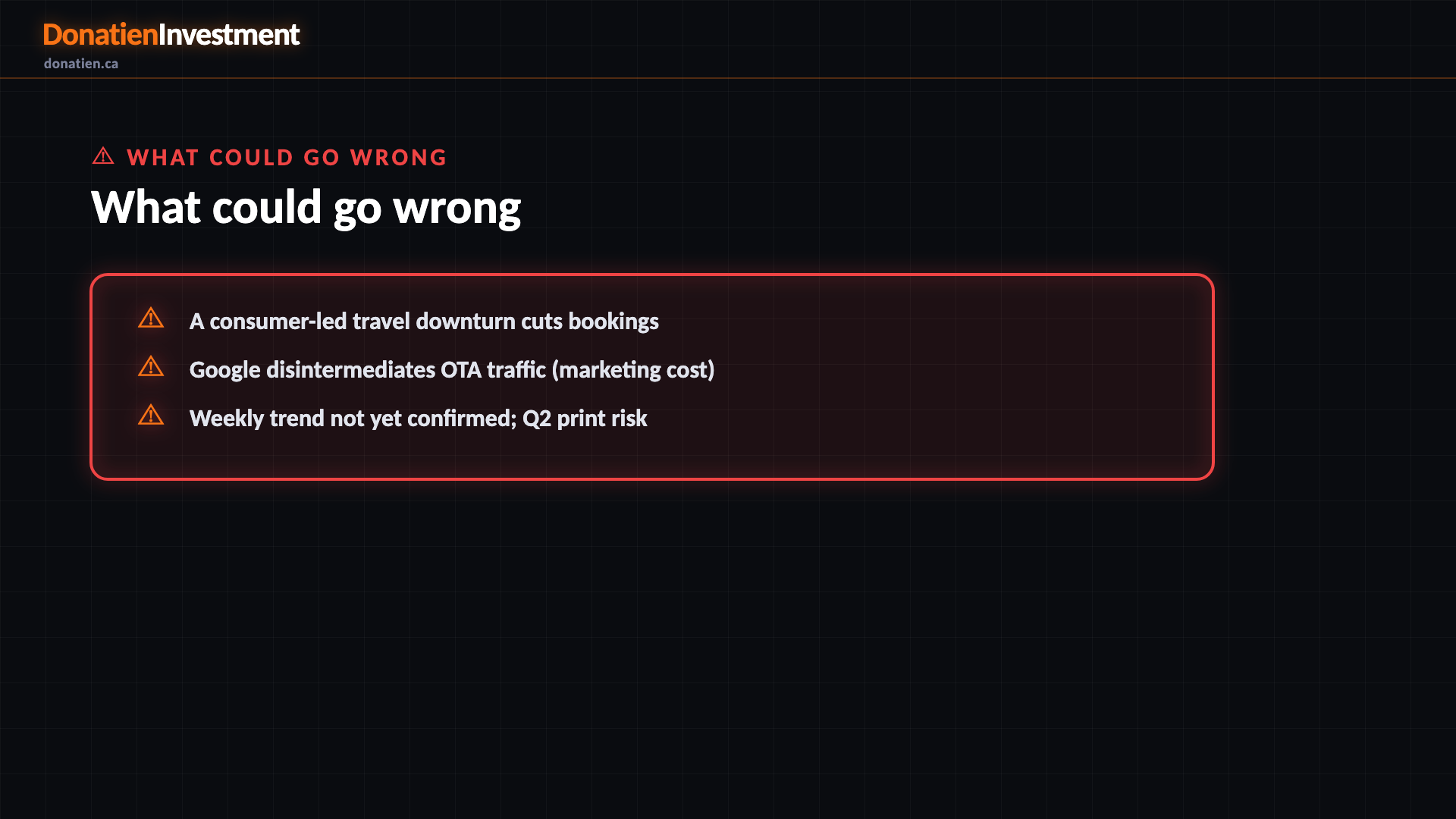

What could go wrong

A consumer-led travel downturn cuts bookings. Google disintermediates OTA traffic (marketing cost). Weekly trend not yet confirmed; Q2 print risk.

Risk vs Reward

The report weights three twelve-month paths with a positive skew. The base case — most likely at 55% — sees Booking around US$210 on steady growth plus buybacks, about fourteen per cent above today. The bull case (25%) reaches US$265 if travel demand stays strong and the multiple re-rates toward the Street. The bear (20%) takes it to US$150 on a travel slowdown or a marketing-efficiency hit — a retest of the May low.

The verdict

The bottom line: a dominant, cash-gushing travel platform at an attractive nineteen times clean earnings, just as the daily chart turns up on volume — a rare value-and-momentum combination, and two of three entry paths are already met. It is a high-conviction BUY, not a strong buy only because the driver and the economy are merely neutral. Sizing around the late-July earnings is prudent.

Read the full report on donatien.ca →{kind=link}

{kind=link}