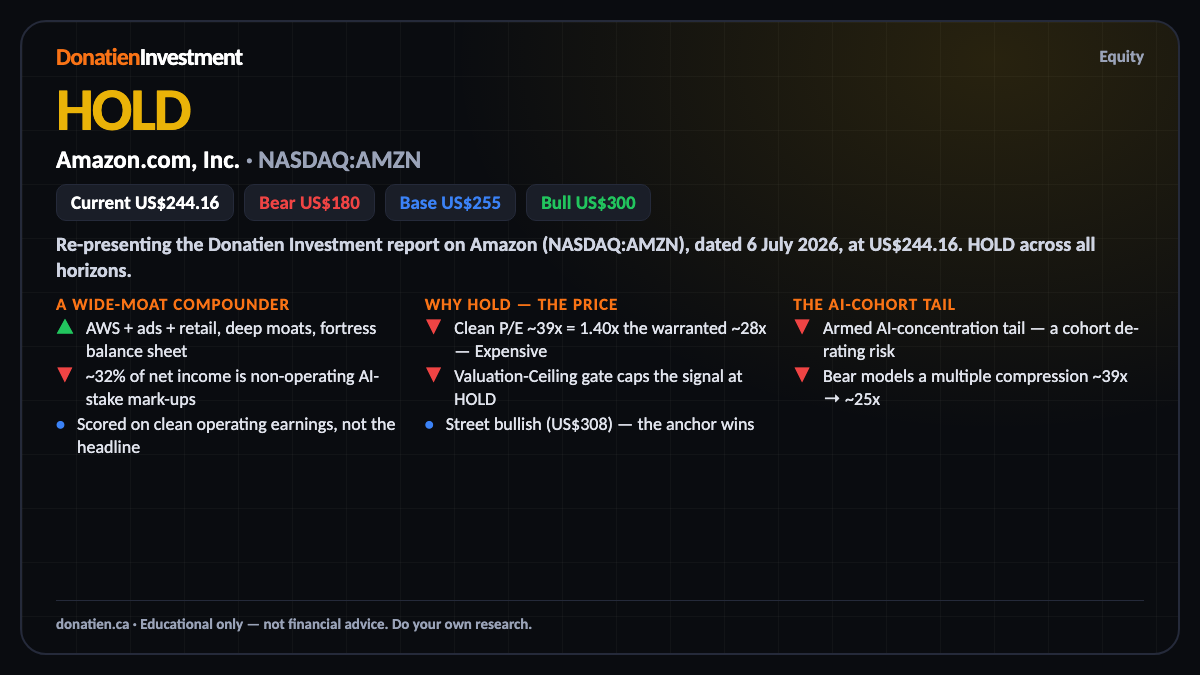

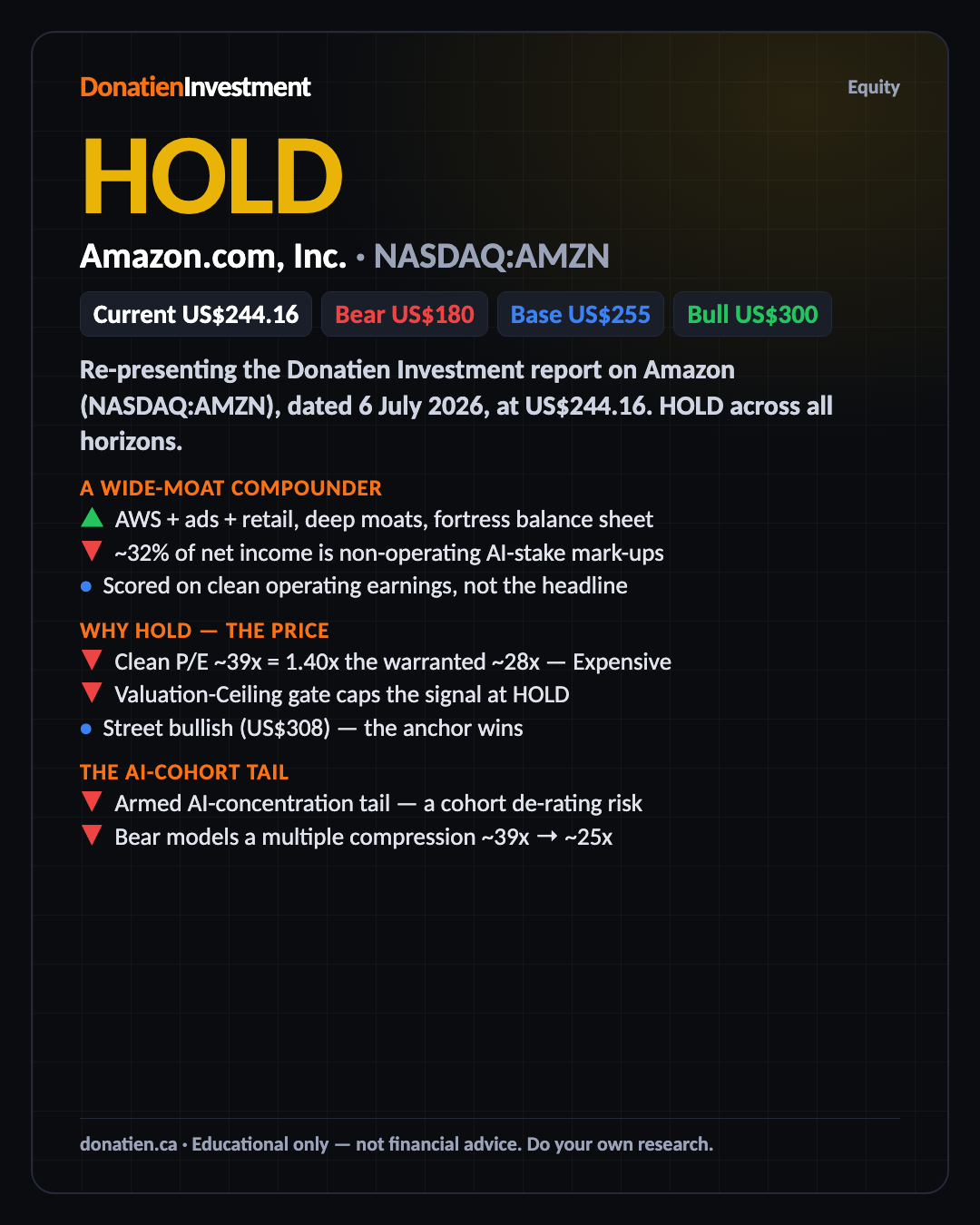

Amazon.com, Inc. (NASDAQ:AMZN) HOLD

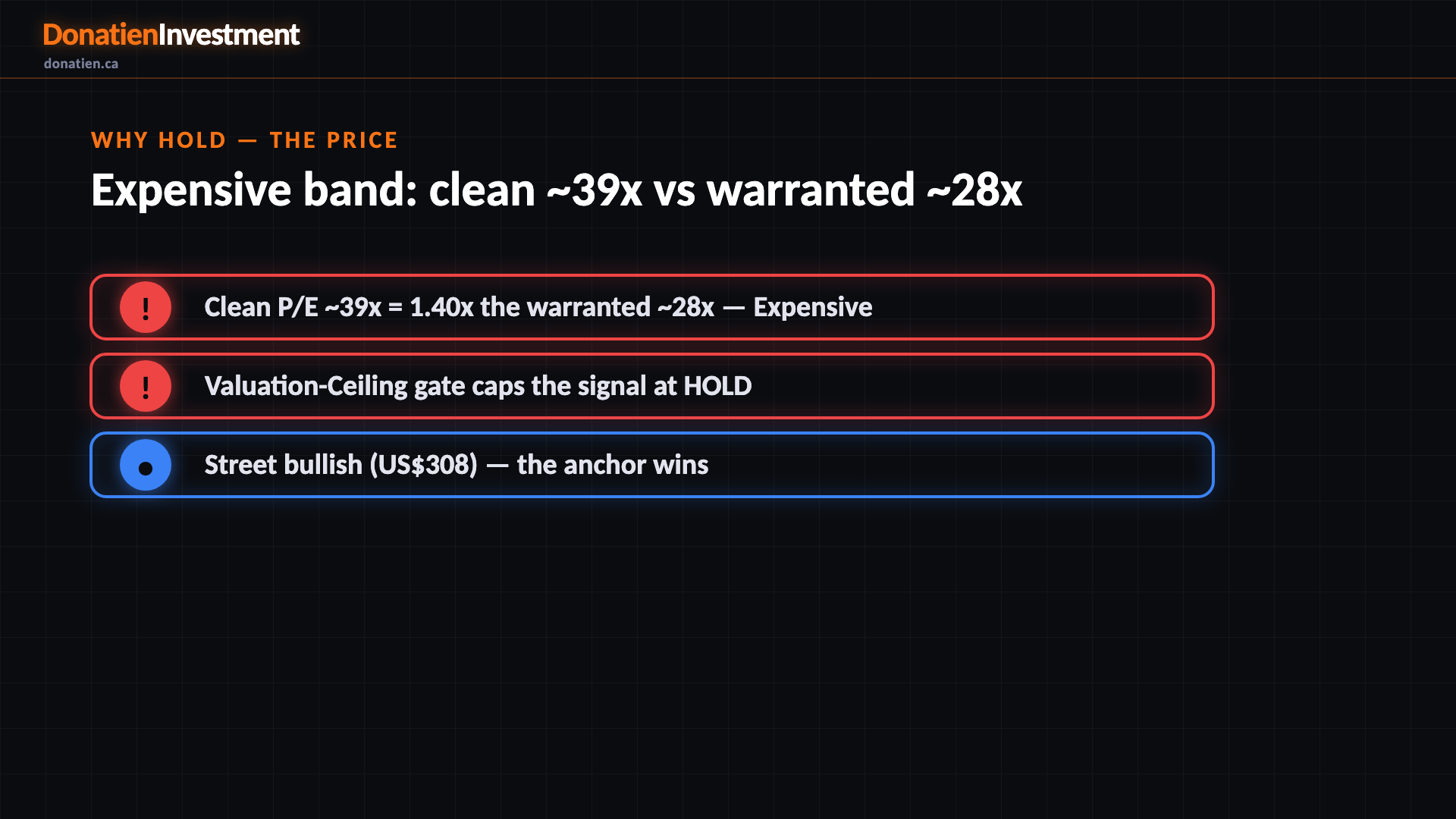

Amazon is a wide-moat cloud, advertising and retail compounder — the quality is not in doubt. But on clean operating earnings it trades around thirty-nine times, roughly forty per cent above what rates and disciplined growth warrant, so it sits in our Expensive band. A great business at a rich price — HOLD.

Re-presenting the Donatien Investment report on Amazon (NASDAQ:AMZN), dated 6 July 2026, at US$244.16. HOLD across all horizons.

A wide-moat compounder

Amazon is a genuinely great business: the largest cloud provider in A-W-S, a fast-growing high-margin advertising arm, and a dominant retail network, all wrapped in deep moats. The one catch on quality is that its reported earnings are flattered — about a third of net income last year was non-operating, mostly mark-to-market gains on its Anthropic stake, spiking to forty per cent in the first quarter. So we score it on clean operating earnings, which is the honest lens.

Why hold — the price

Here is what caps it. On clean earnings Amazon trades around thirty-nine times, against a warranted multiple near twenty-eight from current rates and disciplined growth — that is our Expensive band, and it fires a valuation-ceiling gate that holds the signal at hold regardless of momentum. Wall Street targets are higher, near three hundred and eight dollars, but the disciplined anchor judges the clean multiple against rates, and thirty-nine times is rich even for a business this good.

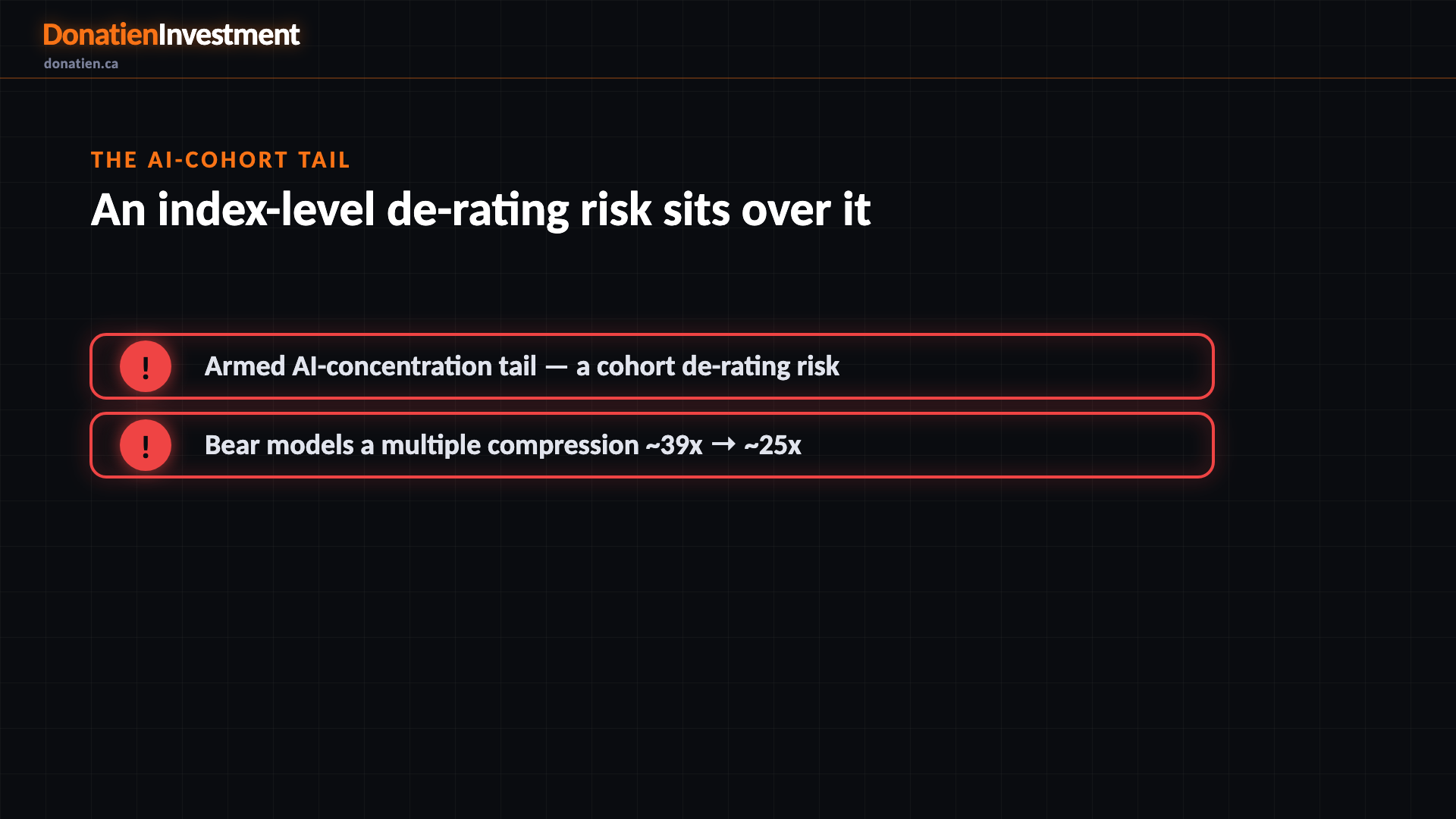

The AI-cohort tail

Amazon also inherits a market-wide risk. The macro report flags an armed concentration tail — a handful of A-I mega-caps on mark-up-inflated earnings leading a cap-weighted index. As a genuine member of that cohort, Amazon's bear case is not just its own fundamentals; it is a cohort-level de-rating, where an A-I private-valuation markdown or a hyperscaler capex cut compresses the multiple from thirty-nine toward twenty-five. That is a much deeper move than the company's own story implies.

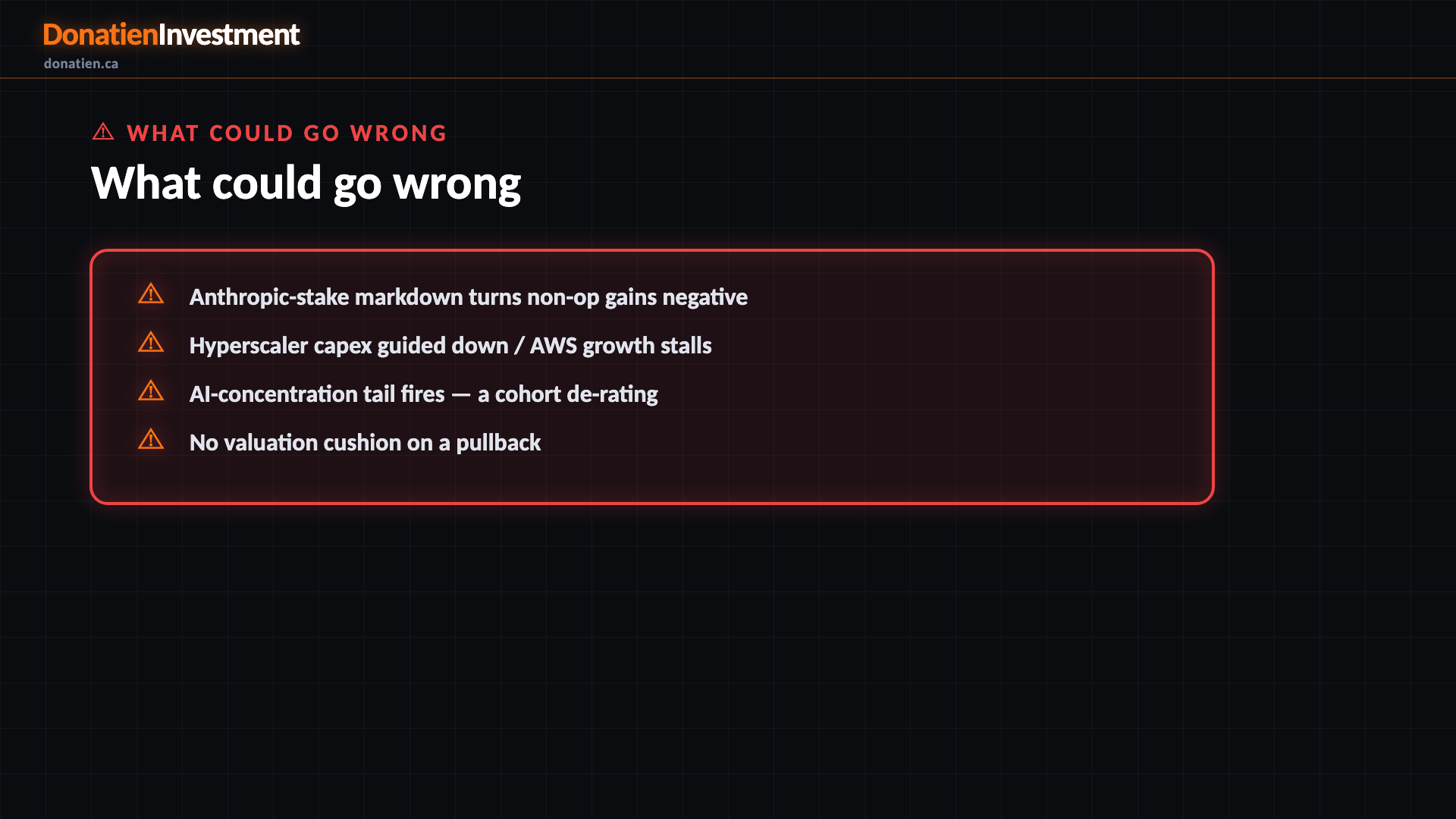

What could go wrong

Anthropic-stake markdown turns non-op gains negative. Hyperscaler capex guided down / AWS growth stalls. AI-concentration tail fires — a cohort de-rating. No valuation cushion on a pullback.

Risk vs Reward

The report weights three twelve-month paths, and the skew is essentially flat. The base case — most likely at 50% — has Amazon around US$255 as solid growth is capped by a rich multiple, only a few per cent above today. The bull case (25%) reaches US$300 if AI monetisation shows up in operating income and the multiple holds. The bear (25%) takes it to US$180 if the AI-concentration tail fires and the clean multiple compresses toward twenty-five times — a cohort-level de-rating, deeper than Amazon's own fundamentals.

The verdict

The bottom line: the quality is not the question — the price is. At thirty-nine times clean earnings, with no valuation cushion and an armed AI-concentration tail over the whole cohort, the risk-reward at this price is poor. It is a hold, not an entry. The edge only opens on a de-rate toward the low-thirties clean multiple, or a genuine step-up in operating earnings.

Read the full report on donatien.ca →{kind=link}

{kind=link}