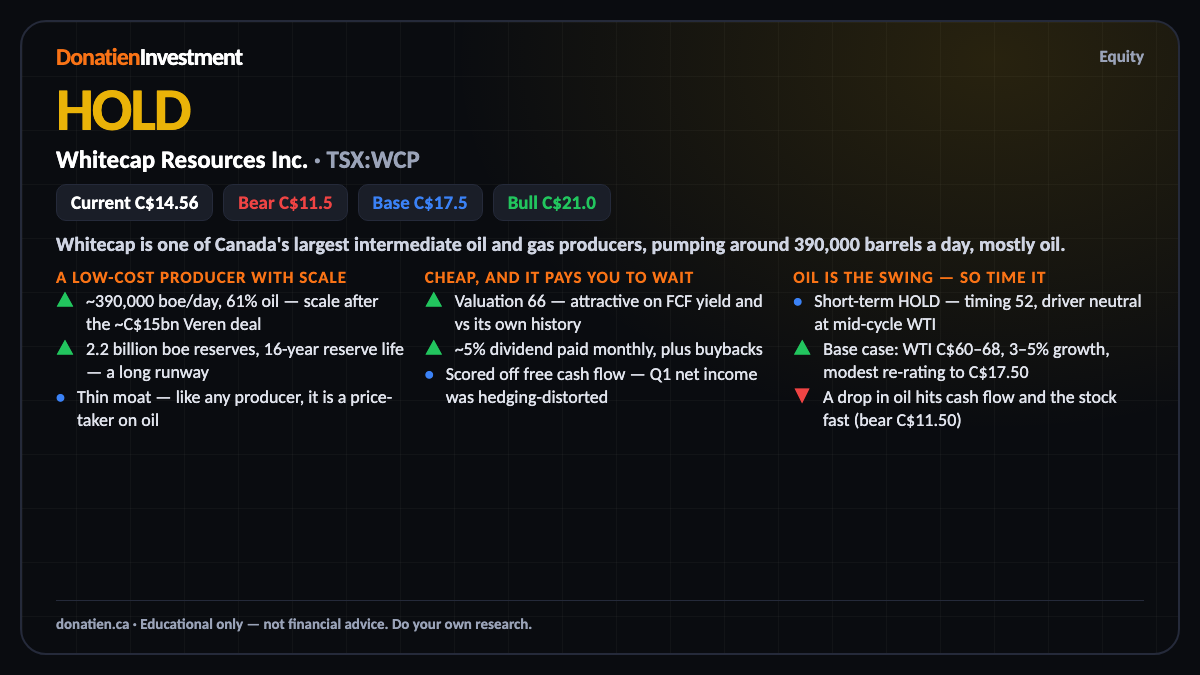

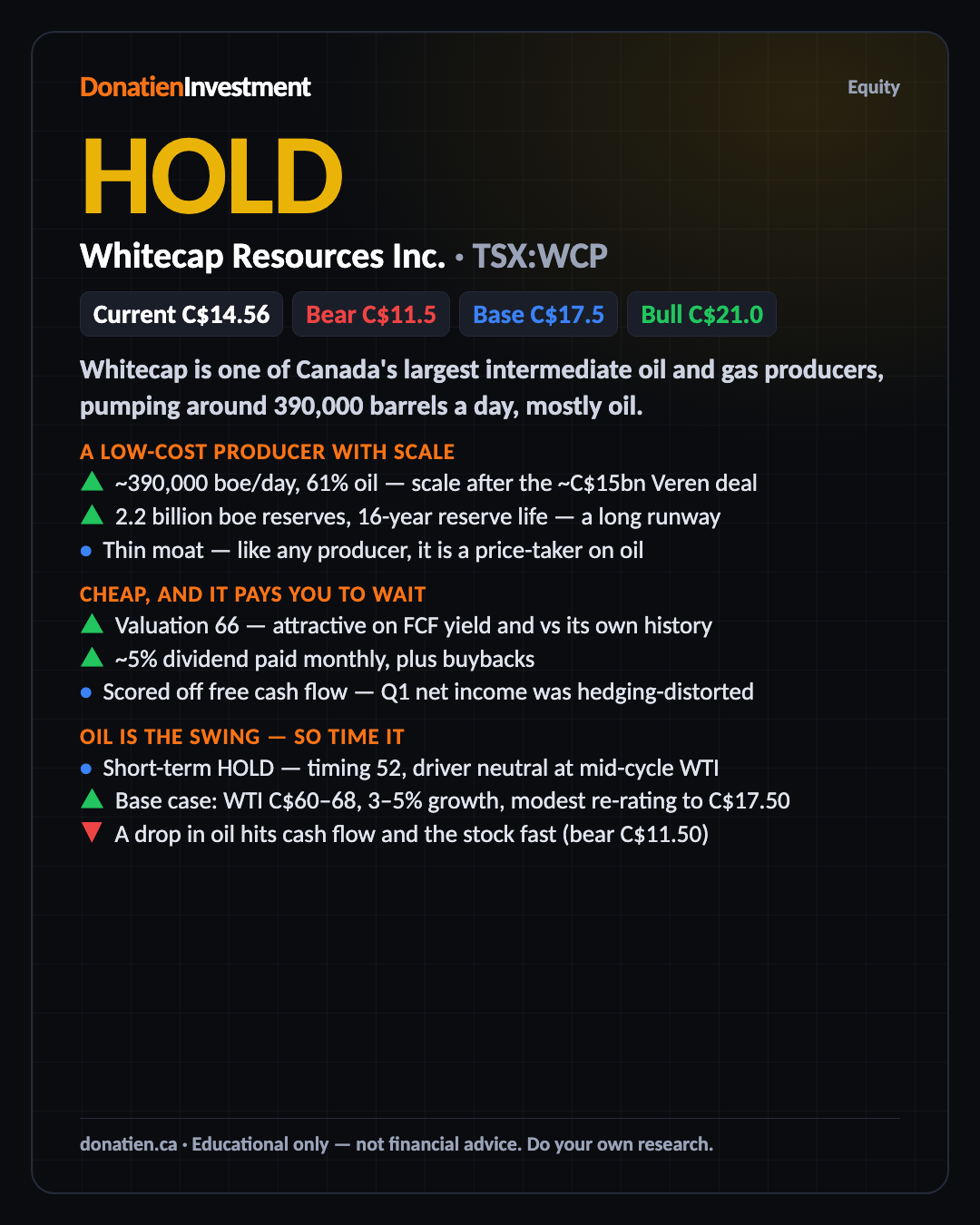

Whitecap Resources Inc. (TSX:WCP) HOLD

Short-term this is a hold — timing is only fair and the oil price, not the company, sets the near-term path. It is a cheap, high-quality producer and a medium- and long-term buy, so accumulate on weakness rather than chase.

Whitecap is one of Canada's largest intermediate oil and gas producers, pumping around 390,000 barrels a day, mostly oil. Last year's ~C$15bn Veren deal roughly doubled it, giving a 2.2 billion-barrel reserve base and a 16-year runway. It returns cash through a monthly dividend and buybacks. The stock is cheap on cash flow — but it is a price-taker on oil, so the entry timing and the crude price are the whole game.

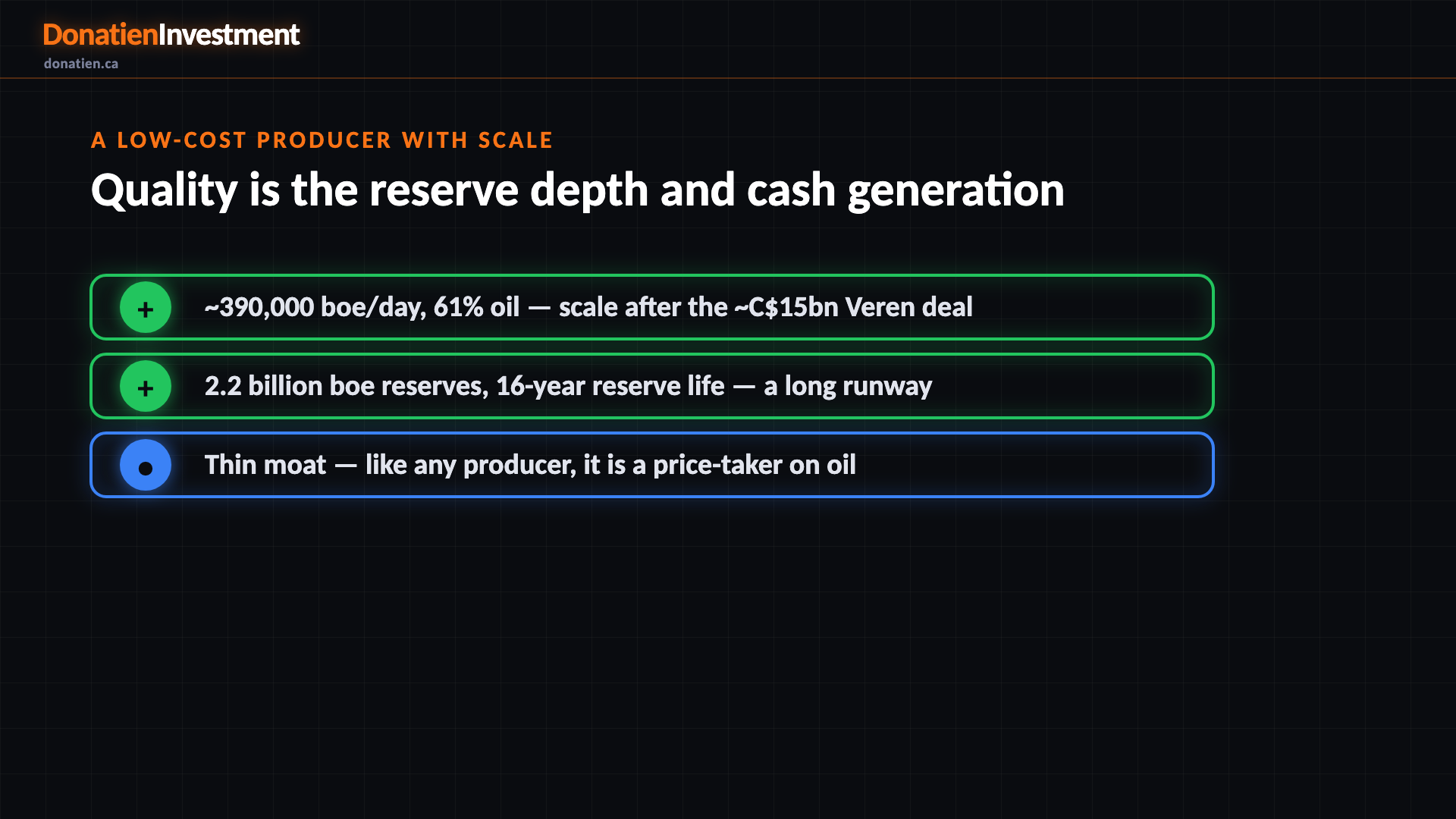

A low-cost producer with scale

Start with the business, because the quality here is scale and staying power. Whitecap pumps around 390,000 barrels of oil equivalent a day, about 61% of it higher-value oil and liquids, from Alberta, British Columbia and Saskatchewan. Last year's roughly C$15bn all-share purchase of Veren nearly doubled the company, leaving it with about 2.2 billion barrels of reserves and a reserve life beyond 16 years — one of the longest runways among its peers. The one permanent limit is the moat: like every producer, it does not set the price of what it sells.

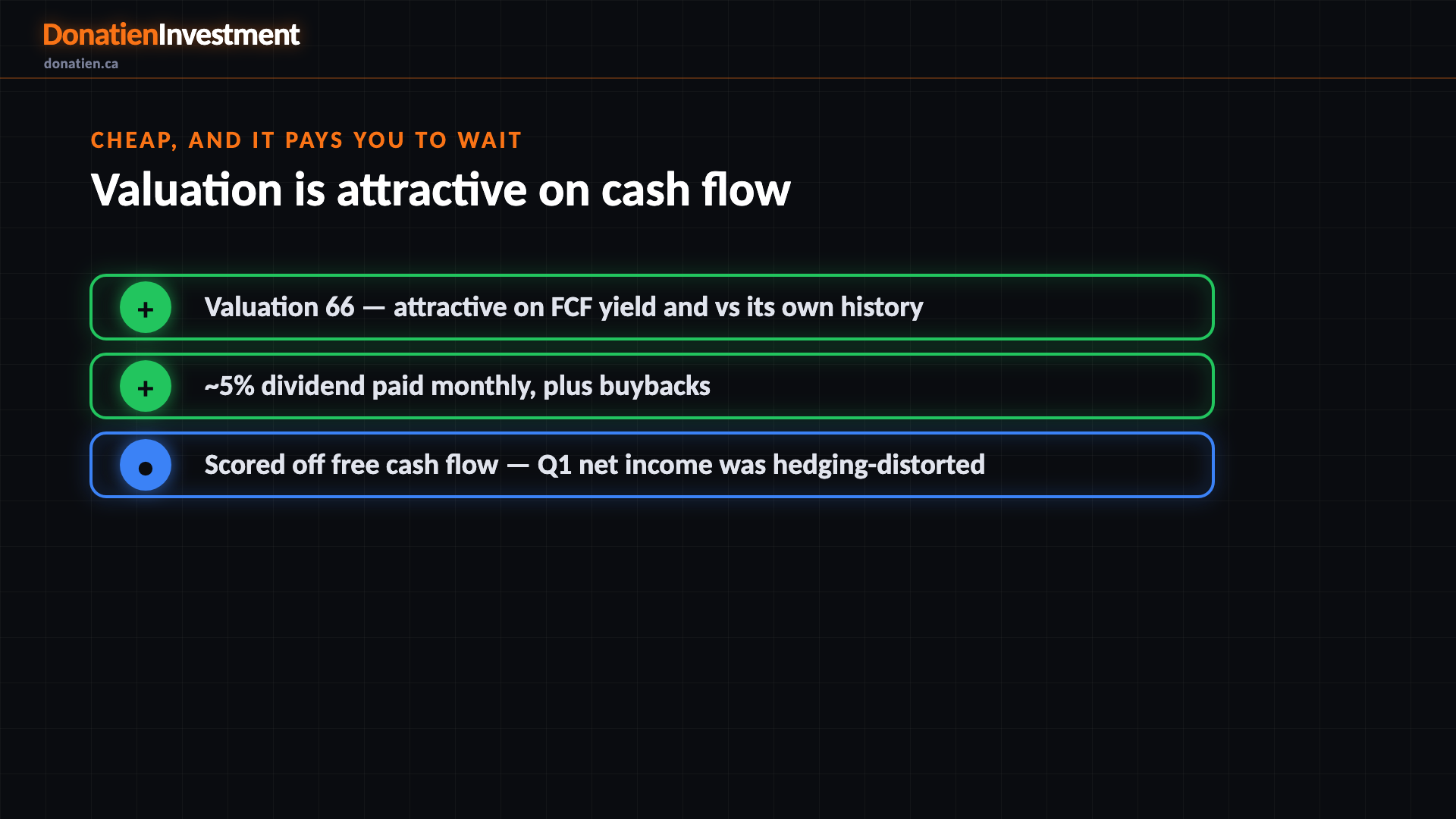

Cheap, and it pays you to wait

On value, it looks cheap and it pays you while you wait. Valuation scores 66 — attractive on free-cash-flow yield and against its own history. The company returns that cash through a monthly dividend of around 5%, topped up by buybacks. One important note on the numbers: last quarter's reported profit was dragged down by a large non-cash hedging loss, so we score it off free cash flow and operating cash flow, not the headline net income — and on that basis the business is comfortably cash-generative.

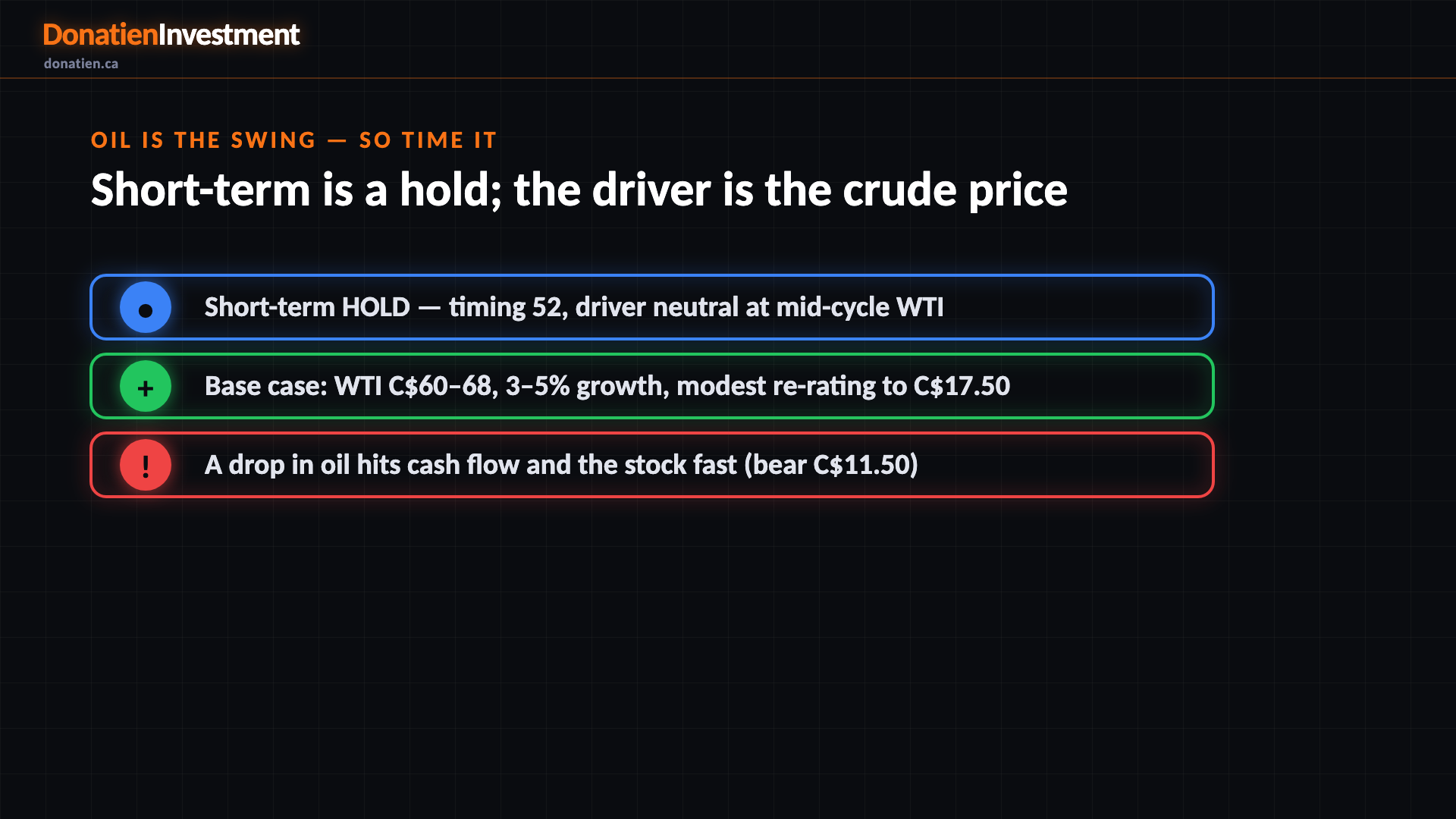

Oil is the swing — so time it

The catch is timing, and it is why the short term is only a hold. The stock is a geared bet on the oil price: the driver sits neutral at a mid-cycle crude level, and short-term timing scores just 52. Our base case assumes WTI around C$60 to C$68, three-to-five percent production growth, and a modest re-rating toward C$17.50. But the same leverage cuts both ways — a sustained drop in oil would hit cash flow and the share price quickly, which is what the bear case near C$11.50 reflects. So accumulate on weakness rather than chase strength.

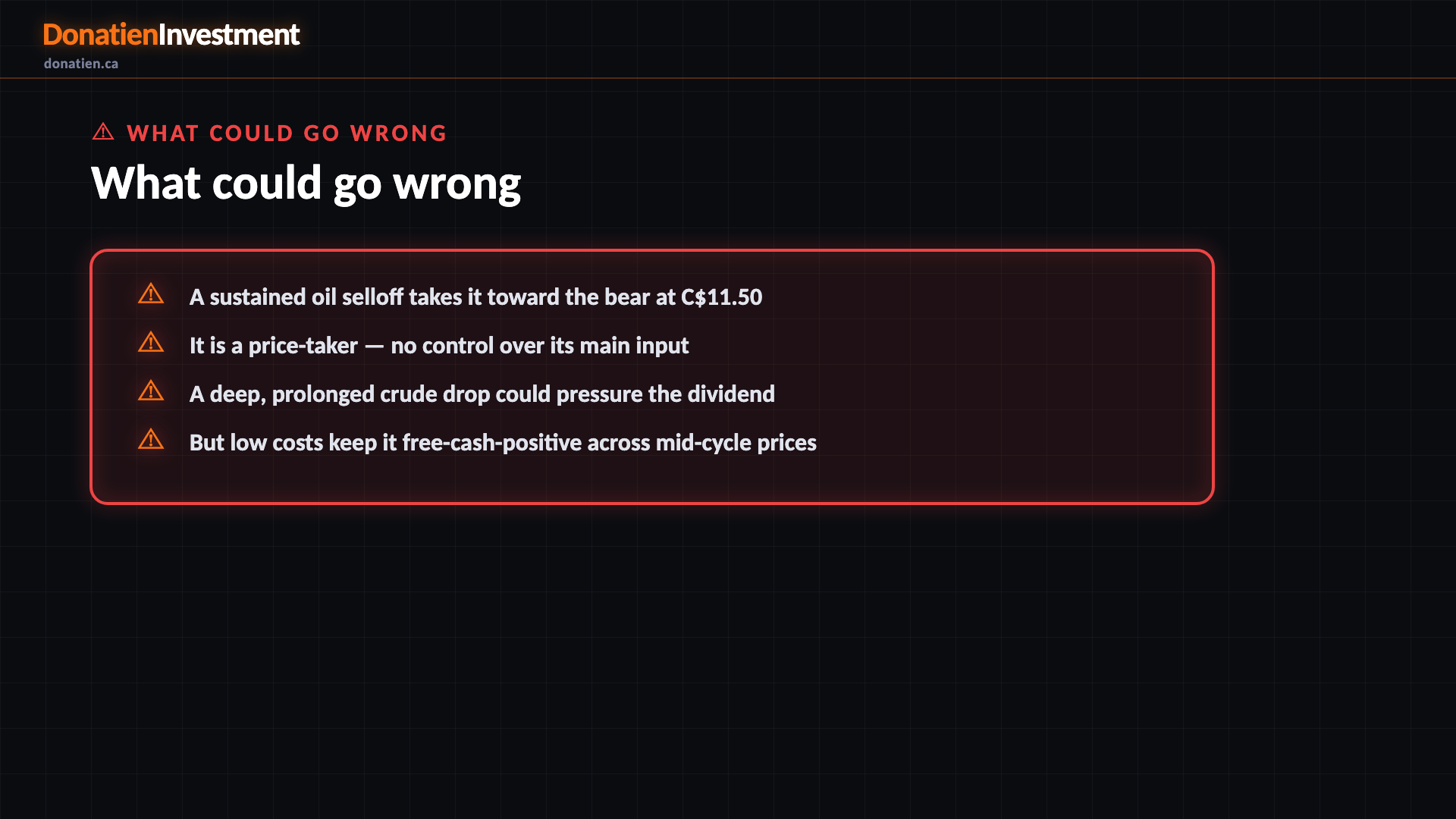

What could go wrong

A sustained oil selloff takes it toward the bear at C$11.50. It is a price-taker — no control over its main input. A deep, prolonged crude drop could pressure the dividend. But low costs keep it free-cash-positive across mid-cycle prices.

Risk vs Reward

The verdict

Hold in the short term — the report's near-term signal is HOLD: timing is only fair and the crude price, not the company, will set the path from here. Underneath, it is a medium- and long-term BUY: a well-run, low-cost oil producer with a long reserve runway, trading cheaply and paying a ~5% monthly dividend. So the honest stance is hold now and accumulate on dips, not chase. The bear case near C$11.50 is an oil-price risk, not a company-quality one.

Read the full report on donatien.ca →{kind=link}

{kind=link}